Futures Contracts Explained Simply for Beginners

A futures contract is one of the simplest derivatives to picture: it is a binding agreement to buy or sell something at a price you fix today, with the actual exchange happening on a set future date. No "maybe", no "if". Both sides are locked in. If you have ever pre-ordered a phone at a locked-in price before it launched, you have felt the spirit of a futures contract — the price is settled now, the delivery comes later.

What is a futures contract?

Strip away the jargon and a future is a promise with four ingredients: what (the underlying asset), how much (the quantity, called the lot size), at what price (agreed today), and when (the expiry date). Once you and a counterparty agree, the deal is fixed for both of you.

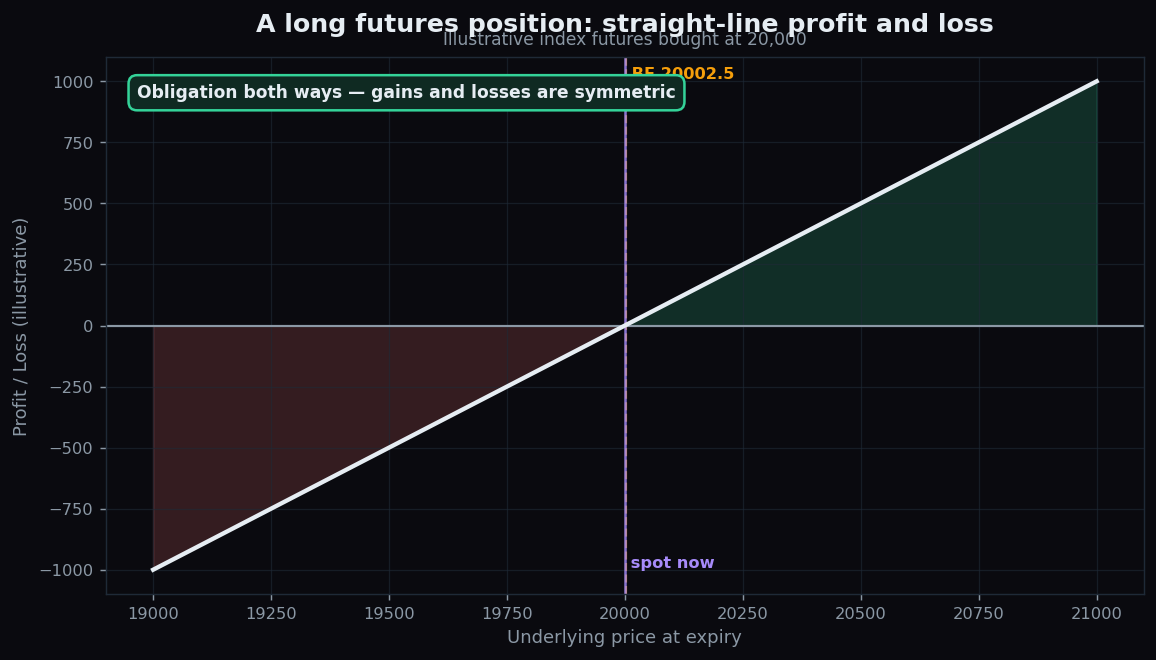

The key word is obligation. A futures buyer must buy at expiry; a futures seller must sell. This is the great divider between futures and options. An option holder can walk away. A futures holder cannot — the commitment binds both directions equally. That is why the profit-and-loss line of a futures position is a straight diagonal: every rupee the underlying moves, your position moves the same, up or down.

A simple worked example

Suppose an index trades at 20,000 and you buy one futures contract at that level, expecting it to rise.

- If the index climbs to 20,300, you gain 300 points (times the lot size).

- If it falls to 19,700, you lose 300 points.

The gain and the loss are mirror images. There is no premium to cushion the downside as there is with options — the symmetry is total. This is an illustration of the mechanics, not a suggestion to trade.

Margin: a deposit, not the full price

Here is where futures become both powerful and dangerous. You do not pay the full value of the contract up front. Instead you post margin — a good-faith deposit, usually a fraction of the contract's total value — that the exchange holds as security.

Imagine that index contract is worth 10 lakh in total value, but the margin required is just 1 lakh. With 1 lakh of capital you are controlling 10 lakh of exposure. That ratio is leverage, and it is the reason futures feel so potent. A 3% move in the index becomes roughly a 30% swing on your deposited margin.

Leverage is a magnifying glass held over your results. It enlarges gains and losses with equal honesty. A small adverse move that a stock investor would barely notice can swallow a large slice of a futures trader's margin.

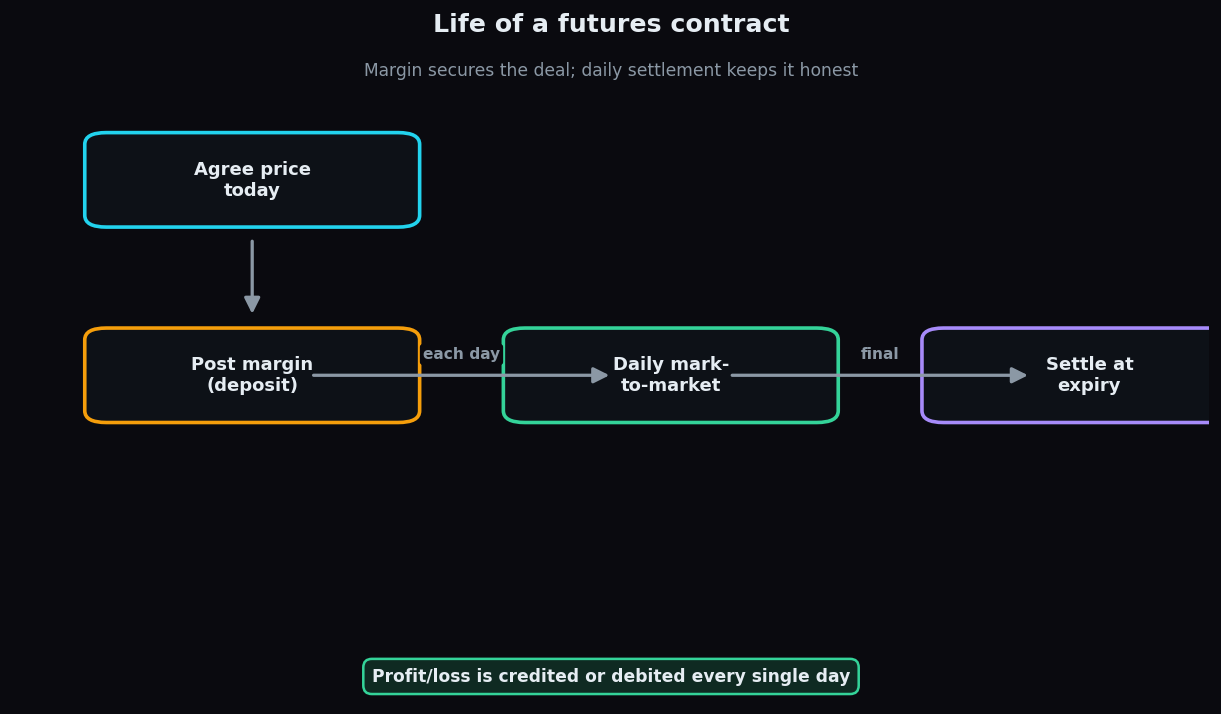

Mark-to-market: settling every single day

You might assume gains and losses are tallied only at expiry. They are not. Futures are settled daily through a process called mark-to-market. At the close of each trading day, the exchange compares the day's settlement price to the previous one and moves money accordingly.

If your position gained today, cash is credited to your account that evening. If it lost, cash is debited. The profit or loss does not wait — it lands in your account day by day.

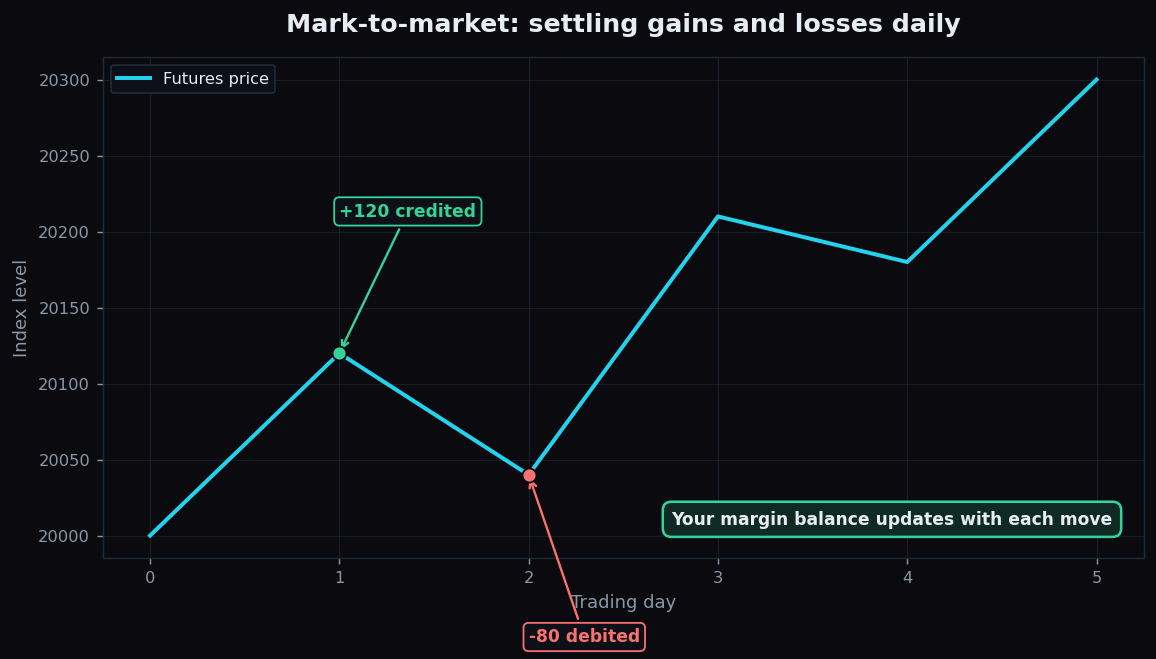

Walk through five days on that 20,000 contract:

- Day 1: price rises to 20,120. You are credited 120.

- Day 2: price slips to 20,040. You are debited 80.

- Day 3: price jumps to 20,210. You are credited 170.

- Day 4: price eases to 20,180. You are debited 30.

- Day 5: price ends at 20,300. You are credited 120.

Add it up and your net is +300 — exactly the difference between your entry of 20,000 and the day-5 price of 20,300. Mark-to-market does not change the final answer; it just settles it in daily instalments instead of one lump at the end.

Why bother? Because daily settlement keeps the system honest. Losses are never allowed to pile up unpaid. If your margin balance falls below a required minimum, you receive a margin call — a demand to top up your deposit. Ignore it, and your position may be closed automatically to protect the exchange from your unpaid loss.

How a futures contract ends

A futures position can finish in three ways. First, you can close it early by taking the opposite trade before expiry — the most common path for short-term traders. Second, you can let it run to expiry and settle, which for index futures in India means cash settlement: no shares change hands, only the final profit or loss. Third, for some stock futures, settlement involves the actual delivery of shares. Most active traders never hold to expiry; they exit beforehand.

The honest catch

Futures are clean and transparent, but they are unforgiving. The same leverage that can multiply a gain can multiply a loss just as fast — and because the obligation is binding, a futures position can in principle lose more than the margin you put down. There is no premium acting as a cap on your downside, unlike a long option.

Daily mark-to-market also means you must keep cash available to meet margin calls, even on a position you firmly believe in. A run of bad days can force you out at the worst moment simply because your margin ran dry. And every contract carries an expiry, so futures are a tool for a defined window, not a buy-and-forget holding. Respect the leverage, keep a buffer, and never deploy more than you can genuinely afford to lose.

Futures move fast, so reading market structure clearly matters more than ever. TrueTrend translates live positioning into plain-language context built for learners. Open a free account and study how the market actually behaves.

Key takeaways

- A futures contract is a binding obligation to buy or sell at a price fixed today on a set expiry date.

- Profit and loss are symmetric — a straight line with no premium to cushion the downside.

- Margin is a small deposit, not the full price; the resulting leverage magnifies gains and losses alike.

- Mark-to-market settles profit and loss daily, and a shortfall triggers a margin call.

- Most traders exit before expiry; index futures in India settle in cash.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.