Futures Rollover Explained: Carrying a Position

Every futures contract has an expiry date. On that day the contract stops existing — it settles and vanishes. But traders often want their position to keep going past that date. So they perform a small two-step manoeuvre called a rollover: they close the contract that is about to expire and simultaneously open the same position in the next month's contract. Done well, it is seamless. Done carelessly, it quietly eats into returns. Here is how it works.

What rollover actually is

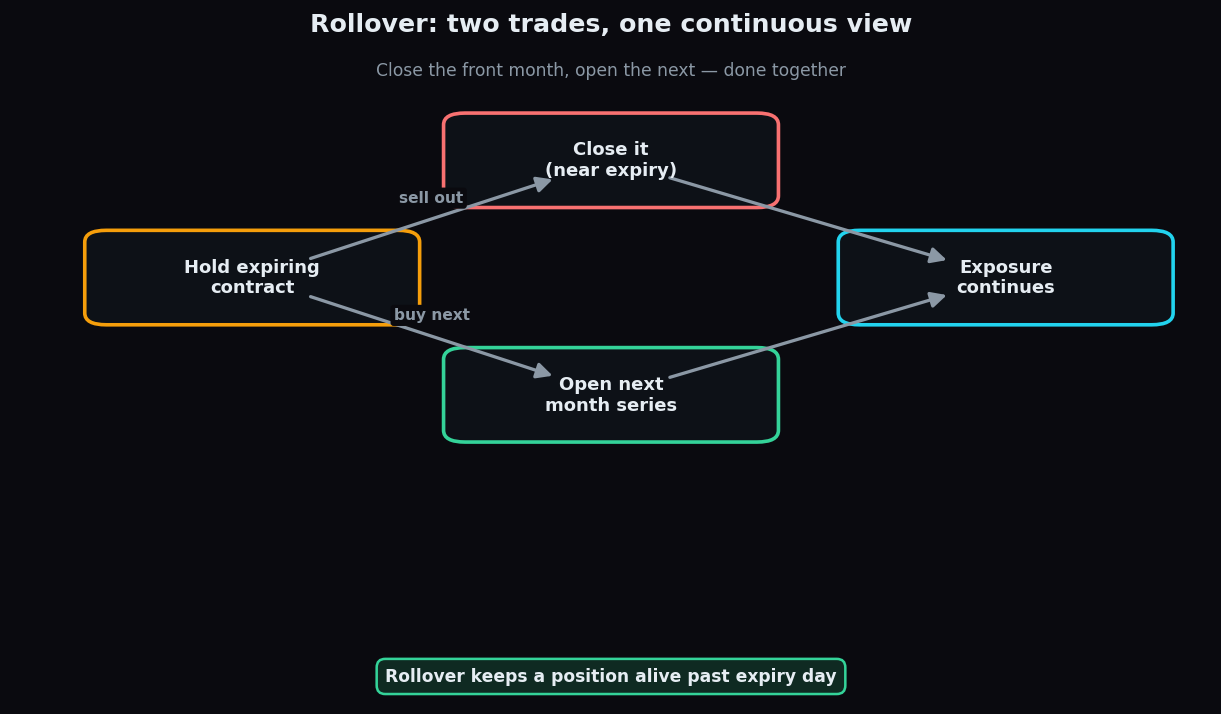

A rollover is the act of moving an open futures position from the expiring contract (the "front month" or "near month") into the next available series (the "next month"). It is not one trade — it is two, executed close together: you square off the near-month contract and open a fresh one in the far month for the same quantity and direction.

The everyday analogy is a magazine subscription. Your current subscription is about to run out. Rather than losing access, you renew for the next period before the old one lapses. Your reading never stops; only the paperwork changes. Rollover does the same for market exposure — the position continues, only the specific contract behind it is swapped.

Why rollover matters

Rollover matters for two reasons. First, practical necessity: if you simply hold a contract to expiry, it settles automatically — in cash for index futures, or by delivery obligations for some stocks — and your directional view ends whether you wanted it to or not. Rolling over is how a longer-term view survives past the monthly deadline.

Second, rollover data is a widely watched sentiment signal. Analysts track the rollover percentage — the share of open positions that traders carry into the next series rather than closing outright. A high rollover percentage suggests participants want to keep their exposure; a low one suggests they are content to let positions expire. It is a descriptive read on conviction, nothing more — not a forecast.

Reading the rollover window

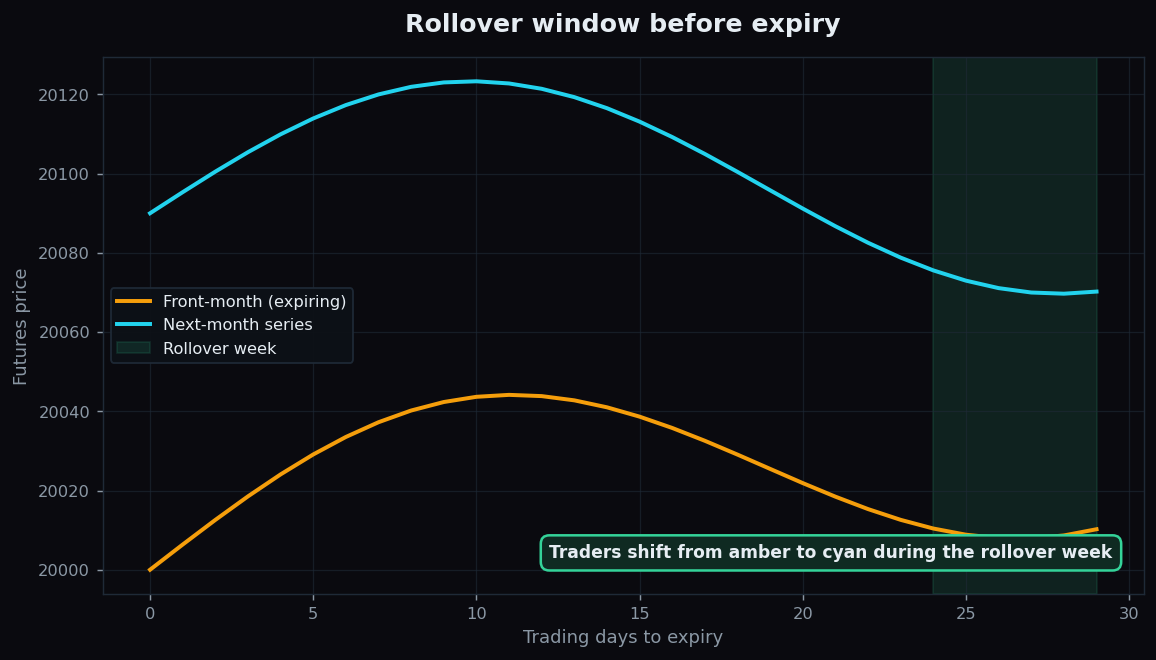

Rollovers cluster in the final few sessions before expiry, a stretch traders informally call the rollover week. During this window the near-month and next-month contracts trade side by side, and activity gradually shifts from the old to the new. The chart below shows both series through that window.

Notice the two lines usually do not sit on top of each other. The next-month contract often trades at a slightly different price than the expiring one — a gap that reflects carrying costs and expectations. That gap is exactly what a rollover has to pay for.

A worked example with round numbers

Suppose you are long one futures contract in the near month, currently priced at 20,000, and the next-month contract is quoting 20,090. These are illustrative numbers.

- You close the near-month long at 20,000.

- You open a new long in the next month at 20,090.

- The 90-point difference is your roll cost — the price of carrying the position forward one month. If instead the next month were cheaper, the roll could work slightly in your favour.

To estimate the rollover percentage, analysts compare how much open interest moved into the next series versus what expired. If, say, 6,00,000 units of open interest existed and 4,50,000 shifted forward, the rollover is roughly 75%. That figure describes how keen participants were to stay in the trade — it does not tell you which way price will go next.

The honest catch

Rollover is routine, but it is not free, and it is not a crystal ball:

- It costs money. You pay the price gap between contracts plus two sets of transaction charges and the bid-ask spread. Roll every month and those costs add up meaningfully over a year.

- Leverage still applies. The new contract carries the same margin and the same amplified risk as the old one — rolling forward does not reduce exposure, it renews it, so losses can keep compounding both ways.

- High rollover is not a buy signal. A crowded rollover simply means many traders kept their positions. Plenty of heavily-rolled trends have reversed. Treat rollover data as context about conviction, not as a prediction.

Expiry-week signals like rollovers make more sense when you can see the whole structure at once. TrueTrend lays out live derivatives context in plain English so you can study it, not chase it. Explore it free.

Key takeaways

- A rollover closes an expiring futures contract and opens the same position in the next series — two trades, one continuous view.

- It exists because contracts settle at expiry; rolling is how a longer-term position survives past the deadline.

- The rollover percentage describes how many positions were carried forward — a read on conviction, not a forecast.

- Rolling costs the price gap between contracts plus transaction charges and spread, which compound over many months.

- The renewed contract keeps the same leverage and risk, so losses can keep compounding in both directions.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.