Futures vs Options: The Key Differences Explained

A futures contract and an options contract both let you take a view on where a price is heading without owning the underlying asset today. But they are built on two completely different promises. One locks you into a deal you must honour. The other hands you a choice you can walk away from. Confusing the two is one of the most expensive beginner mistakes in the derivatives market, so let us pull them apart carefully.

What each one actually is

A future is an obligation. When you buy a futures contract, you agree to buy the underlying — an index, a stock, a commodity — at a set price on a future date. The seller agrees to deliver at that price. Both sides are bound. Think of it like booking a wedding caterer at a fixed rate months ahead: whatever food prices do later, both you and the caterer must go through with the deal at the agreed number.

An option is a right, not a duty. A call option gives the buyer the right to buy at a set price (the strike); a put gives the right to sell at the strike. The buyer pays a fee called the premium for this right and can simply let it expire worthless if it is not useful. Think of it like a refundable token you pay to reserve a price — if the deal turns sour, you lose only the token, not the whole purchase.

Why the difference matters

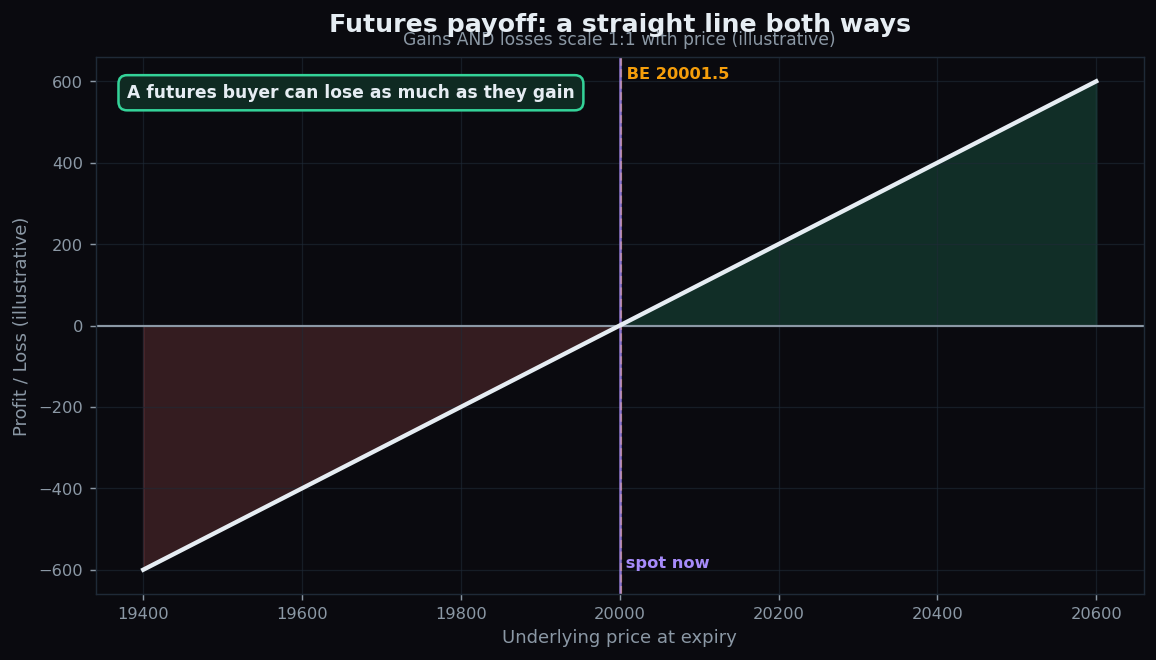

The obligation-versus-right distinction changes the entire risk profile — the shape of what you can gain and lose. With a future, the payoff is a straight line. If the price rises, your gain grows point for point. If it falls, your loss grows just as fast, in the same straight line. There is no natural floor.

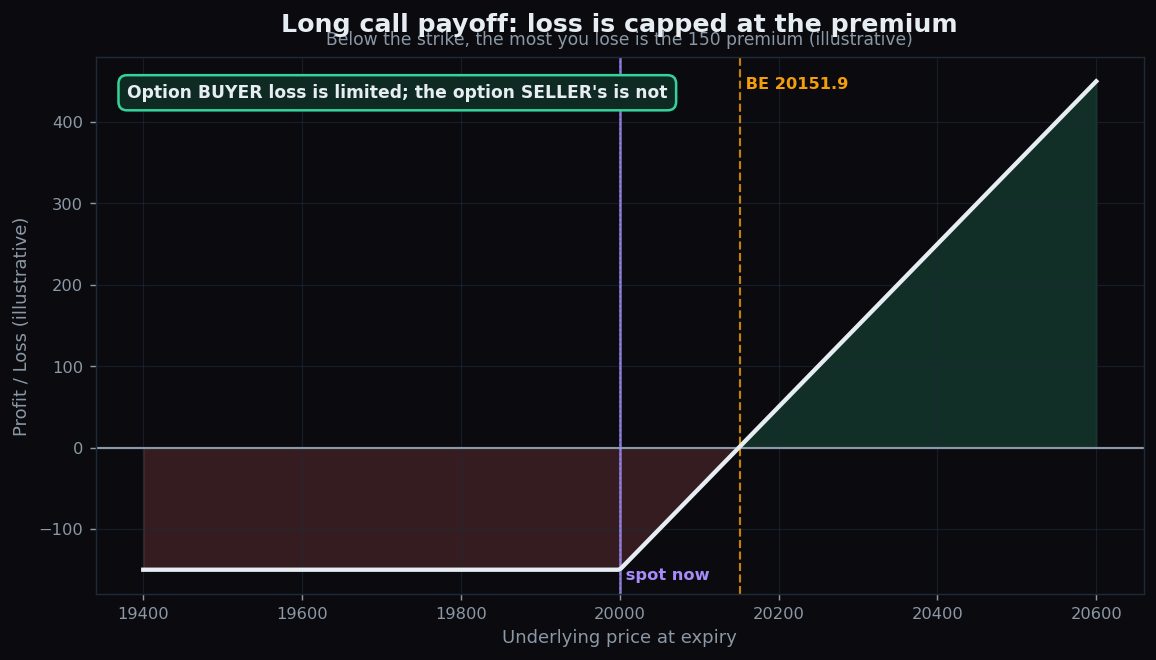

An option buyer has a bent payoff instead. Below the strike a call buyer simply loses the premium and nothing more, while above the strike the gains can keep climbing. That bend — limited loss, open-ended gain — is the headline appeal of buying options.

How they are used in practice

Both instruments are traded on margin and in standard lots (a fixed quantity per contract), so a relatively small amount of money controls a large notional value. People use futures when they want clean, symmetric exposure — a direct one-to-one bet on direction, often to hedge an existing holding. People buy options when they want defined risk: the most a buyer can lose is known the moment the trade is placed. Sellers (also called writers) of options take the opposite side, collecting the premium in exchange for accepting large, open-ended risk — closer in spirit to the futures seller.

A worked example with round numbers

Say an index sits at 20,000 and you expect it to rise. These are illustrative figures, not a recommendation.

- Futures route: You buy one futures contract at 20,000. If the index climbs to 20,300, you gain 300 points times the lot size. If instead it drops to 19,700, you lose 300 points times the lot size. Symmetric — the upside and the downside are mirror images.

- Option route: You buy a 20,000 call for a premium of 150. If the index falls to 19,700, you lose only the 150 premium, full stop. If it climbs to 20,300, your option is worth about 300 at expiry, so your net gain is 300 minus 150, or 150 per unit. You gave up some profit in exchange for a hard floor on your loss.

Notice the trade-off: the future gave a bigger raw gain on the same move, but it also exposed you to a bigger raw loss. The option cost you the premium up front but capped the damage.

The honest catch

Neither instrument is "safer" in a blanket sense. A future feels simple, but because it moves point for point with full leverage, a sharp adverse move can wipe out your margin and demand more — losses can exceed your initial deposit. An option buyer enjoys capped loss, but options carry time decay: the premium erodes a little every day, so even if the price never moves, a buyer can slowly bleed to zero. And the option seller faces the same open-ended risk as a futures trader, sometimes worse. Leverage cuts both ways in every one of these structures. The right tool depends entirely on the risk you can genuinely absorb, not on which one sounds clever.

Understanding payoff shapes is the first step to reading the market like a professional. TrueTrend turns raw derivatives data into plain-English context so you can study structure instead of guessing. Create a free account to explore.

Key takeaways

- A future is an obligation with a straight-line payoff: gains and losses scale equally and there is no built-in floor.

- An option is a right; the buyer's loss is capped at the premium, while the upside on a call stays open.

- Futures usually cost more in margin; options cost a premium that decays over time.

- Option sellers carry large, open-ended risk — closer to the futures profile than to the option buyer.

- Leverage amplifies both gains and losses in every one of these structures; match the tool to the risk you can truly afford.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.