Growth vs Value Investing: Two Honest Philosophies

Walk into any room of investors and you will eventually hear the friendly argument: is it better to buy fast-growing companies, or cheap ones? These two camps — growth investing and value investing — have debated the point for decades. This article explains both honestly, because the useful answer is not “pick a side.” It is understanding what each approach is really betting on, and where each one tends to trip.

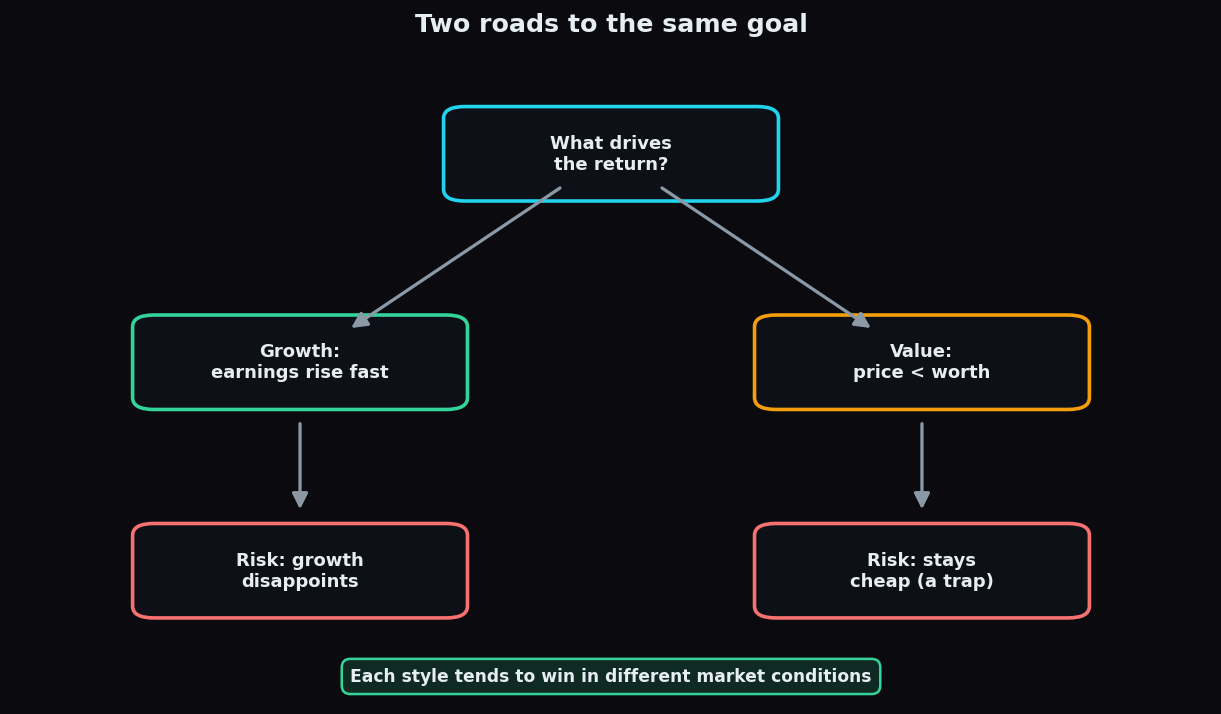

Two philosophies, one goal

Both styles want the same thing: to end up with more money than they started with. They just take different roads there.

- Growth investing looks for companies whose sales and profits are expanding quickly, and is willing to pay a rich price today in the belief that tomorrow’s much larger business will justify it.

- Value investing looks for companies trading below what the buyer estimates they are actually worth, aiming to buy a rupee of business for less than a rupee and wait for the gap to close.

The key terms, defined

A few pieces of jargon show up constantly, so let us pin them down:

- P/E ratio (price-to-earnings) — the share price divided by earnings per share. It roughly says how many rupees investors pay for each rupee of annual profit. A high P/E means the market expects strong future growth.

- P/B ratio (price-to-book) — the share price divided by the company’s book value (assets minus liabilities) per share. A low P/B can suggest the stock is cheap relative to what the company owns.

- Margin of safety — a value investor’s buffer: buying well below the estimated worth so that even if the estimate is wrong, losses are limited.

An everyday analogy

Picture two shoppers at a bazaar. The growth shopper spots a small stall that is packed every single day and getting busier; she happily pays a premium for a stake, betting it becomes the biggest stall in the market. The value shopper walks past a quiet, unglamorous shop selling solid goods at a marked-down price; he buys precisely because it is cheap and expects others to notice its worth eventually. Both can be right. Both can be wrong. They are simply reading different signals.

A worked example with round numbers

Imagine two fictional companies, each with a share price of ₹500.

- QuickServe Ltd earns ₹10 per share and grows sales about 30% a year. Its P/E is 500 ÷ 10 = 50. Investors pay up because they expect earnings to multiply.

- SteadyMetals Ltd earns ₹50 per share and grows slowly. Its P/E is 500 ÷ 50 = 10, and it pays a regular dividend.

A growth investor is drawn to QuickServe, accepting the high P/E as the price of rapid expansion. A value investor prefers SteadyMetals, paying far less per rupee of current profit and collecting dividends while waiting. Notice that neither is “cheating” — they are pricing in completely different expectations about the future. (Numbers are illustrative only.)

Where each approach can go wrong

Every honest description of a strategy includes its failure mode:

- Growth’s danger is disappointment. When a company priced for 30% growth grows only 10%, the high P/E can collapse, and the fall is often sharp because so much optimism was baked into the price.

- Value’s danger is the value trap: a stock is cheap for a good reason — a fading industry, weak management, shrinking demand — and it simply stays cheap, or gets cheaper. Low price alone is not a bargain.

Neither is universally “better”

Decades of market history show growth and value taking turns. In some periods, low interest rates and exciting new industries reward growth handsomely; in others, rising rates and a hunger for steady cash flow reward value. Because no one reliably predicts which period comes next, many investors deliberately hold some of both, and the line between the styles is blurrier than the debate suggests — a wonderful growing business bought at a sensible price is, in a sense, both. The takeaway is not to crown a winner but to know which bet you are making and why.

Whichever style appeals to you, the habit that matters most is understanding the mechanics behind the labels. To keep building that literacy with clear, no-hype explainers, you can explore TrueTrend by creating a free account.

Key takeaways

- Growth investing pays a premium for fast-expanding companies; value investing buys companies priced below their estimated worth.

- Growth leans on metrics like a high P/E and rapid sales growth; value leans on a low P/E, low P/B and a margin of safety.

- Growth’s risk is that growth disappoints; value’s risk is the value trap — cheap for a real reason.

- The two styles outperform in different market conditions, and no one reliably predicts the switch.

- Neither is inherently better; the point is to know which bet you are making, and many investors blend both.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.