Lot Size and Contract Value in F&O Explained

When you buy a share, you can buy exactly one, or seven, or 143 — any number you like. But step into the futures and options market and that freedom disappears. Here you can only trade in fixed bundles called lots. You cannot buy half a lot or a lot and a quarter. This single rule quietly shapes how much money you need, how much risk you carry, and why F&O is not a beginner's playground. Let us unpack it.

What a lot is

A lot is the smallest standard quantity of an underlying that one derivatives contract represents. The exchange fixes it in advance for every instrument. One index contract might equal 50 units of the index; one stock contract might equal 250 or 1,000 shares. You trade in whole lots — one, two, three — never a fraction.

Think of buying eggs. The shop does not sell you a single egg; it sells trays of, say, 30. If you want eggs, you buy a tray, or two trays, but not 47 loose eggs. The tray is the trading unit. In derivatives, the lot is that tray — a standard bundle everyone agrees to deal in.

Contract value: the number that surprises beginners

The contract value — also called the notional value — is what one whole lot is actually worth in the market. The formula is refreshingly simple:

Contract value = lot size × price of the underlying.

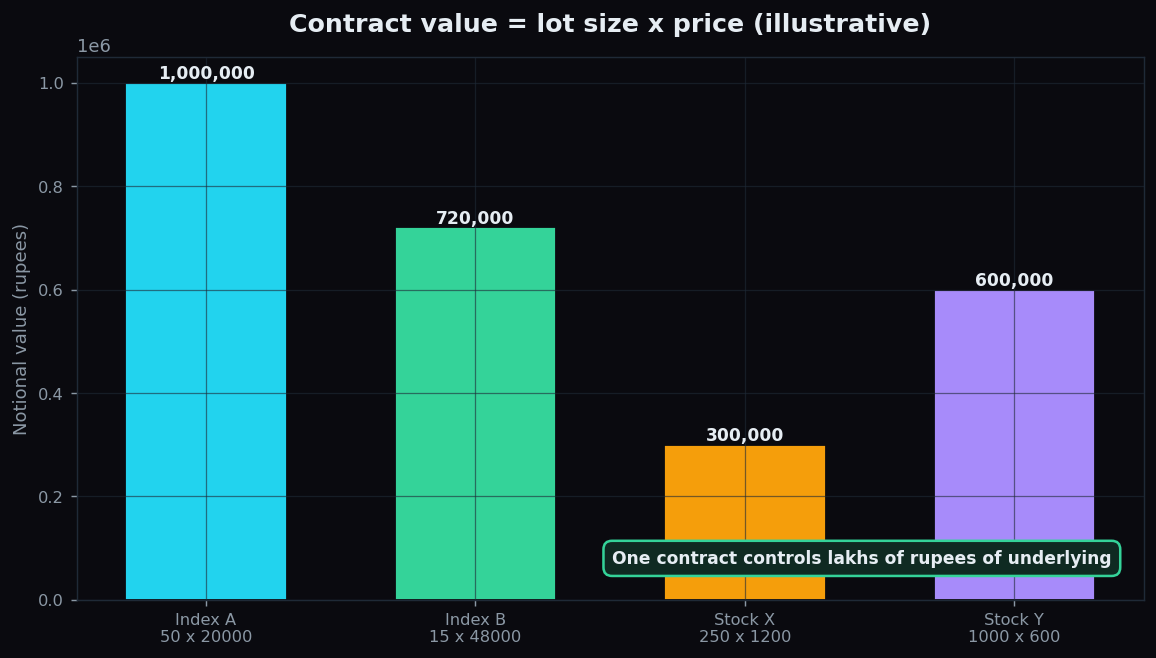

This is where newcomers get a shock. Because a lot bundles many units together, even a single contract can be worth several lakh rupees. The chart below shows a few illustrative contracts and the notional value each one controls.

Every one of those bars represents one contract. You are not dealing in a few thousand rupees of exposure — you are controlling lakhs. That is the reality the lot size hides in plain sight.

A worked example with round numbers

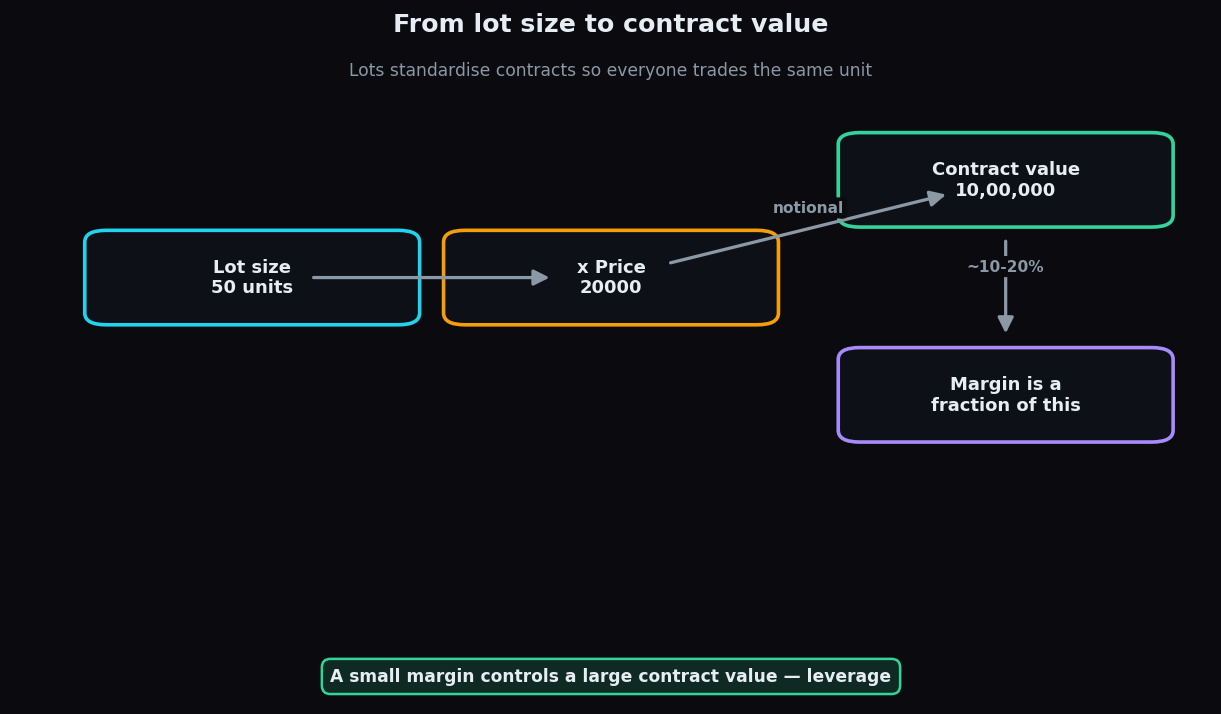

Suppose an index trades at 20,000 and its lot size is 50. These are illustrative figures.

- Contract value = 50 × 20,000 = 10,00,000. One contract controls ten lakh rupees of the index.

- You do not pay the full ten lakh. You post margin — a deposit that might be, say, 10–20% of the contract value, so roughly 1,00,000 to 2,00,000.

- Now watch the leverage. If the index moves just 1%, from 20,000 to 20,200, that is 200 points. On 50 units that is a 10,000 change in your position — a large swing relative to your margin, in either direction.

So the lot size does two things at once: it sets the size of your bet, and — because margin is only a slice of the contract value — it quietly determines how much leverage you are carrying.

Why lot sizes exist at all

Lot sizes are not there to annoy small traders. They serve real purposes:

- Standardisation. When every contract represents the same fixed quantity, buyers and sellers can match instantly without haggling over amounts. A liquid, orderly market needs everyone trading identical units.

- Meaningful contract size. Exchanges deliberately set contract values large enough that the market is used by serious participants and small enough to stay tradeable. This is also a mild gatekeeper — F&O is designed for those who can genuinely absorb the risk.

- Cleaner settlement. Fixed lots make clearing, margining, and expiry handling far simpler than arbitrary quantities would.

From time to time exchanges revise lot sizes — usually to keep the contract value within a target band as prices drift. If a stock rises sharply over the years, its lot size may be cut so one contract does not become unmanageably large.

The honest catch

The lot system has a blunt consequence that beginners must respect. Because one lot already controls a large notional value, your smallest possible position is still big. There is no "dip a toe in" option — the minimum bet is a full lot, and a full lot on margin means real leverage. A modest move in the underlying can produce a large gain or a large loss on your deposit, and that risk cuts equally in both directions. Sizing a single lot correctly — asking whether you can absorb a bad move on the full contract value, not just the margin — matters far more than most newcomers assume.

Knowing what one lot really controls is the first step to trading it responsibly. TrueTrend presents live contract context in plain English so you can study the real size of a position before you act. Get started free.

Key takeaways

- A lot is the fixed, standard quantity one derivatives contract represents; you trade whole lots only.

- Contract value = lot size × price — so a single contract often controls lakhs of rupees.

- You post only margin, a fraction of the contract value, which is exactly what creates leverage.

- Lot sizes exist for standardisation, sensible contract size, and clean settlement; exchanges revise them as prices move.

- Because even one lot is large and leveraged, a small price move can mean a big gain or loss — size positions against the full contract value.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.