Max Pain Theory Explained: The Strike Where Value Expires

Max pain is one of the most talked-about — and most misunderstood — ideas in options. The name sounds ominous, and the theory sounds almost conspiratorial. In plain terms, max pain is just the strike price at which the largest rupee value of options would expire worthless. This guide explains the mechanics with a synthetic example, then spends just as long on why you should hold the idea loosely.

What max pain claims

Every option that finishes out-of-the-money at expiry expires worthless — the holder gets nothing, and the writer keeps the premium. Max pain is the single expiry price at which the combined value of all those worthless options is largest, meaning option buyers collectively collect the least. Put the other way round, it is the price that would cause the most total “pain” to the people holding options, hence the name.

The folklore attached to it goes further: it suggests price has a tendency to gravitate toward the max-pain strike as expiry approaches, supposedly because option writers are motivated to see the most contracts expire worthless. Hold on to that word supposedly — we will come back to it.

How the strike is found

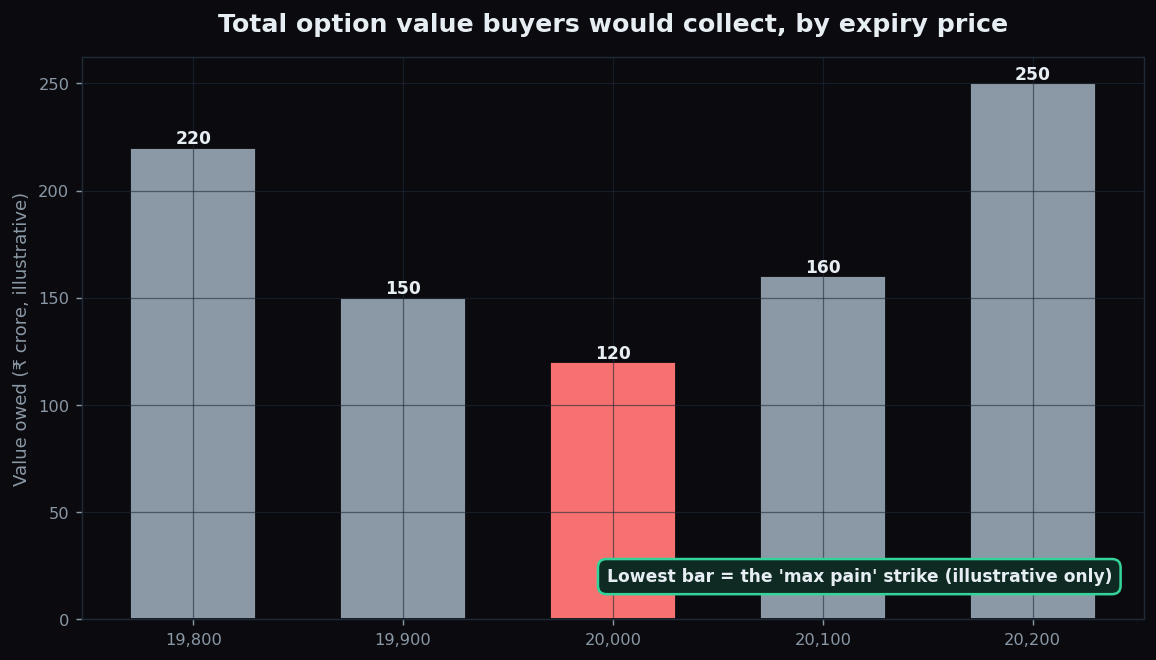

The calculation is mechanical. For each possible expiry price, you add up how much value option holders would be owed across every strike — call value plus put value. Then you look for the price where that total is smallest. That minimum point is the max-pain strike.

The bars above show a synthetic example. At an expiry of 19,800 or 20,200, buyers would be owed a lot of value (220 and 250 crore in made-up units). At 20,000, the total drops to its lowest point of 120 crore. So in this illustration, 20,000 is the max-pain strike.

A worked example

Keep it simple with round numbers. Imagine only two strikes have meaningful open interest:

- 19,800 puts: 100 lakh units are open.

- 20,200 calls: 100 lakh units are open.

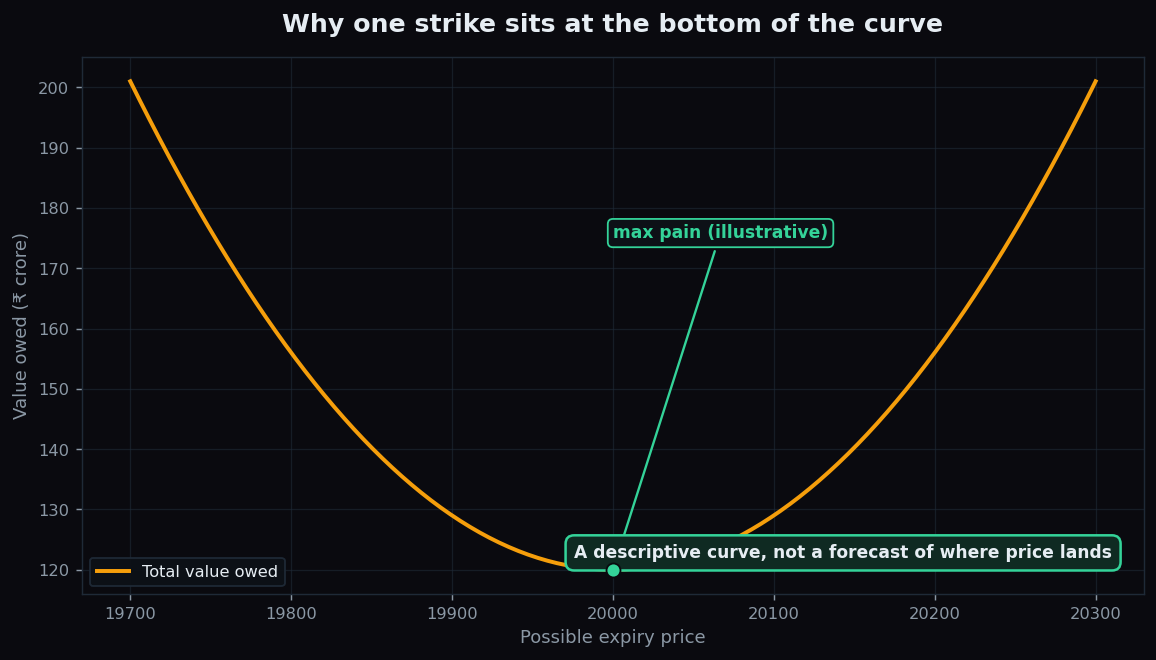

If the underlying expires at 20,000, both of those positions finish out-of-the-money. The 19,800 puts are worthless (price is above 19,800) and the 20,200 calls are worthless (price is below 20,200). Total value owed to holders from these two strikes: zero. Push expiry down toward 19,800 and those puts start paying out; push it up toward 20,200 and those calls do. Because option writers collectively prefer the smallest total payout, the balancing point — where the combined owed value is lowest — sits between the clusters. In a real option chain with many active strikes (like the chart above), that balance lands on one strike: the max-pain point. That is all the “curve” below is doing.

The honest catch — read this part twice

Max pain is a tidy description of where option value concentrates. As a prediction of where price will land, it is weak, and the caveats matter more than the theory:

- Correlation is not causation. Price sometimes closes near max pain at expiry, but that can happen simply because open interest naturally clusters around the current price. The strike did not pull the price; both were shaped by the same market.

- The “writers manipulate price” story is largely a myth. No single group can reliably steer a liquid index into a chosen strike, and rigorous studies find the pinning effect is small, inconsistent, and mostly limited to the final hours.

- It moves as OI moves. The max-pain strike is recalculated constantly and can jump around during the week, so it is a shifting description, not a fixed target.

- It ignores everything else. News, earnings, and macro moves routinely blow price far past any max-pain level.

The safest way to hold max pain is as a piece of context: it shows where option value is densest right now. It is not a forecast, and it is certainly not a reason to act on any position.

TrueTrend presents option-structure context like this in plain language, always paired with its caveats, so beginners learn the idea without the hype. Create a free account to explore it.

Key takeaways

- Max pain is the expiry price where the largest rupee value of options would expire worthless — the point where holders collectively collect the least.

- You find it by adding up value owed to holders at each possible price and picking the lowest total, as in the chart.

- In the worked example, out-of-the-money clusters on both sides push the minimum toward 20,000.

- The pinning story is weak: correlation is not causation, and studies find any effect is small and mostly last-hour.

- Treat max pain as descriptive context about where option value sits — never as a price forecast or an instruction.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.