The Power of Compounding Explained Simply

Albert Einstein probably never actually called compounding the eighth wonder of the world — but the quote stuck around because the idea really is that powerful. Compounding is the simple engine behind almost every story of patient wealth-building, and yet most people underestimate it badly. This post explains what it is, why time matters more than the size of your returns, and where the idea can quietly mislead you. All numbers below are illustrative — round figures chosen to teach the mechanics, not forecasts of anything.

What compounding actually is

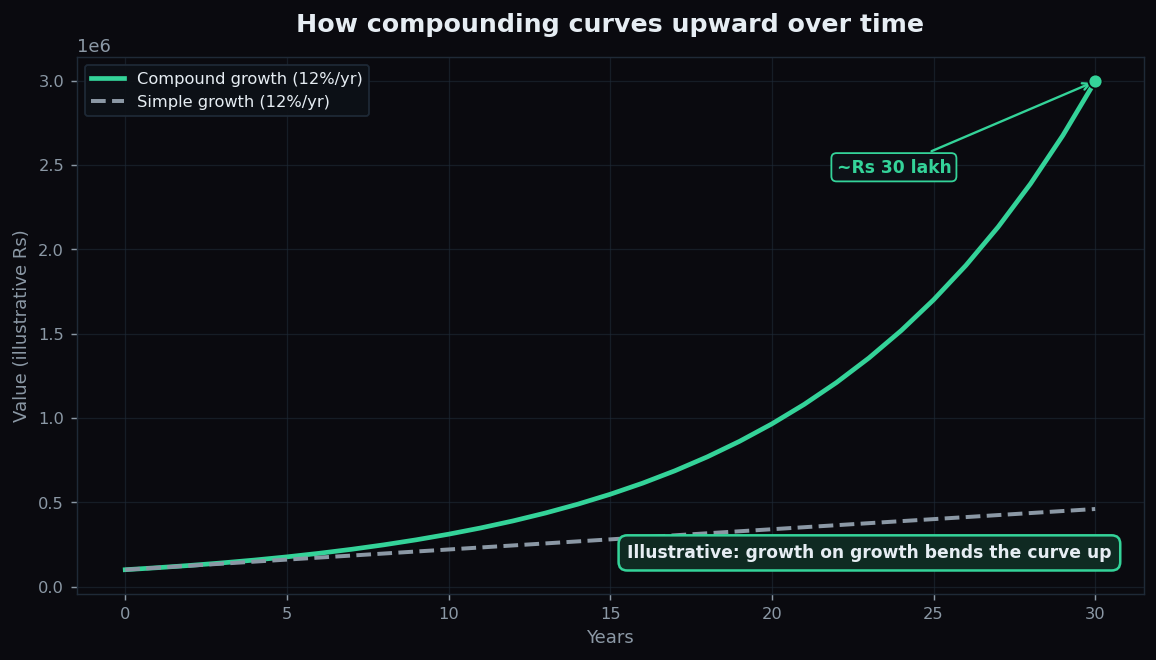

Compounding means earning returns not just on your original money, but also on the returns you have already earned. Your gains start making their own gains. That is the whole trick — and it is why the growth curve bends upward instead of climbing in a straight line.

Compare it with simple interest, where you earn a fixed amount each period only on the original sum. Simple interest draws a straight line. Compounding draws a curve that starts slow and then accelerates.

Think of a snowball rolling downhill. At the top it is tiny and barely moves. But every turn adds a layer of snow, and each new layer makes the ball bigger, so the next layer is bigger too. Near the bottom the same snowball is enormous and gathering mass fast. Your money behaves the same way: the early years look boring, the later years look almost unfair.

A worked example with round numbers

Say you put in Rs 10,000 and it grows a tidy 10% a year (an illustrative rate, not a promise).

- Year 1: 10,000 grows by 1,000 → Rs 11,000.

- Year 2: now 11,000 grows by 1,100 (10% of the bigger number) → Rs 12,100.

- Year 3: 12,100 grows by 1,210 → Rs 13,310.

Notice the interest itself keeps rising: 1,000, then 1,100, then 1,210. Nobody added fresh money — the earlier gains are now earning too. Stretch that same 10% out over 30 years and the Rs 10,000 becomes roughly Rs 1,74,000. Over 40 years, about Rs 4,52,000. The last decade adds far more than the first, even though the rate never changed.

Why time matters most

Here is the part people miss. In compounding, the length of time your money stays invested usually matters more than squeezing out a slightly higher return. Time is the ingredient that lets the curve reach its steep part.

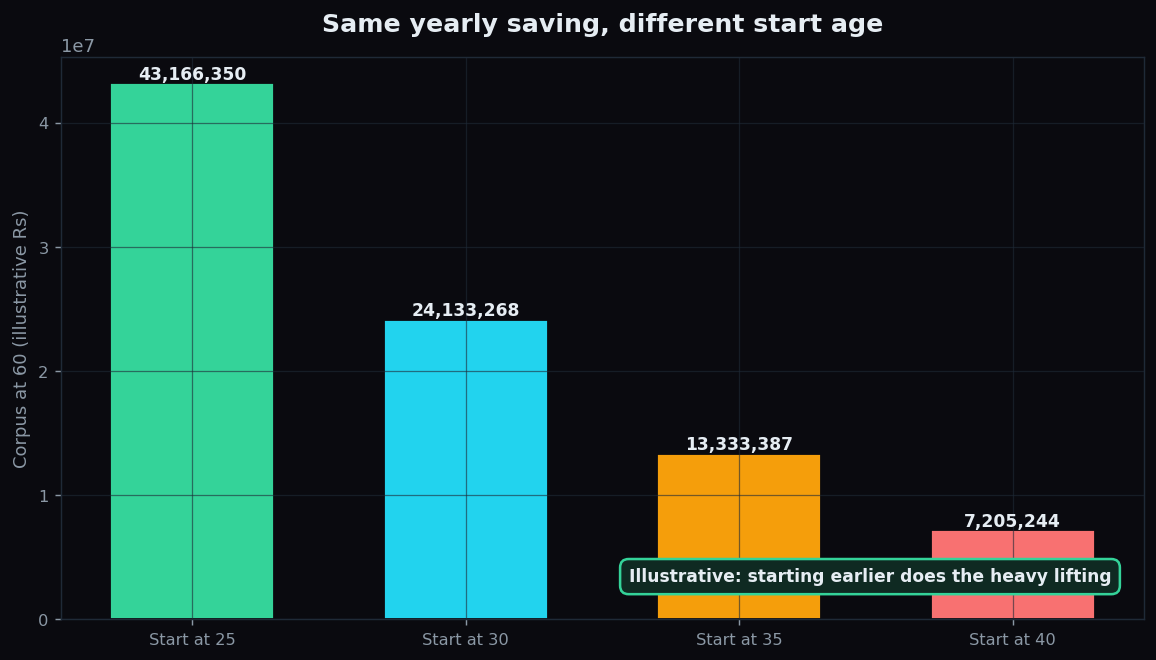

Picture two savers who each set aside the same amount every year until age 60. One starts at 25; the other waits until 35. Those extra ten years at the start land in the steepest part of the curve, so the early starter can finish with a dramatically larger pile — often close to double — despite contributing for only ten more years. The chart above shows this illustrative gap. The lesson is not about any specific number; it is that starting sooner gives compounding more room to work.

A handy shortcut is the Rule of 72: divide 72 by your annual return to estimate how many years it takes money to double. At 12% a year, 72 ÷ 12 = 6 years to double (illustrative). At 8%, it is nine years. The rule is a rough mental tool, not a precise formula, but it shows how a higher rate — or simply more time — shortens each doubling.

How the idea is used

Compounding shows up far beyond a savings account:

- Reinvested dividends. When a company pays a dividend and you reinvest it rather than spend it, those units earn future dividends too.

- Systematic investing. Regular monthly contributions each get their own runway of compounding, so money added early works the hardest.

- Debt — in reverse. Compounding is not always your friend. Credit-card balances compound against you: unpaid interest gets added to the balance, and next month you pay interest on that interest.

- Skills and habits. The mental model even fits learning — small daily gains stack on top of each other. That is an analogy, not a financial claim, but it explains why the concept feels universal.

The honest catch

Compounding is real, but the tidy textbook curve hides some important truths.

- Real returns are not smooth. Markets do not hand out a neat 10% every year. Some years are up, some are sharply down. A bad stretch early on can dent the base that everything later compounds from.

- Inflation eats the curve. If your money grows 10% but prices rise 6%, your real gain is closer to 4%. Always separate the headline number from purchasing power.

- Costs and taxes compound too. A fee of just 1% a year, or taxes on frequent churn, quietly compounds against you and can shave a meaningful slice off the final figure over decades.

- Interruptions hurt. Pulling money out and restarting resets the snowball to a smaller size. The magic depends on leaving it alone.

None of this cancels the idea — it just means the fantasy version (a perfectly straight 12% forever) is not how the world works. The direction of the lesson survives: give money time, keep costs low, and avoid breaking the chain.

Understanding how time and consistency shape outcomes is the quiet foundation of market literacy. TrueTrend builds beginner-friendly, plain-English explainers and a transparent public scoreboard so you can learn the mechanics before you ever risk a rupee. Explore the tools and start free at TrueTrend.

Key takeaways

- Compounding means earning returns on your past returns, which bends the growth curve upward over time.

- The early years feel slow; the later years do the heavy lifting — like a snowball rolling downhill.

- Time in the market often matters more than a slightly higher return; starting earlier gives the curve room to steepen.

- The Rule of 72 (72 ÷ rate) is a quick way to estimate doubling time.

- Real life is messier: volatility, inflation, fees, and taxes all compound too — some for you, some against you.

- All figures here are illustrative teaching examples, not forecasts or advice.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.