Top-Down vs Bottom-Up Analysis Explained

When someone sets out to research a stock, they usually start from one of two ends. Some begin with the big picture — the economy, interest rates, which industries are thriving — and work down to a single company. Others begin with the company itself — its products, profits and management — and worry about the wider world later. The first path is called top-down analysis; the second, bottom-up. Neither is right or wrong. They are two lenses on the same market, and understanding both makes you a sharper reader of it.

What the two approaches are

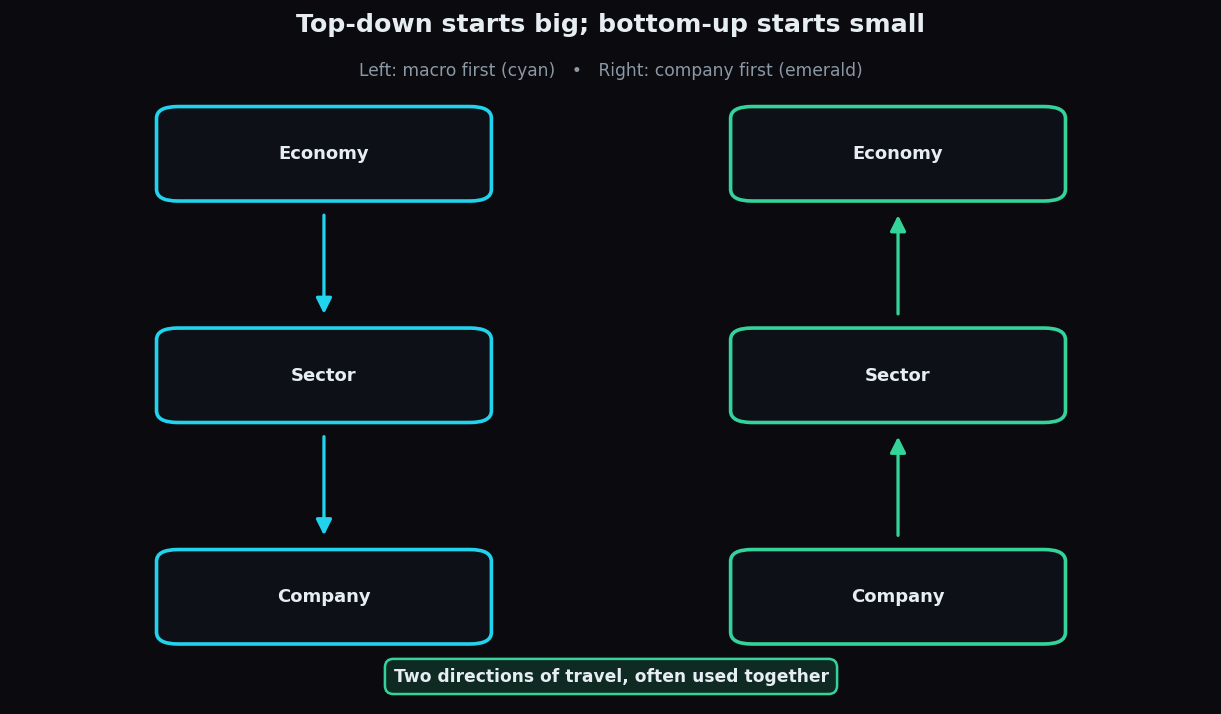

Top-down analysis starts at the widest level and narrows. First the analyst asks: where is the whole economy heading — growing or slowing, inflation rising or falling, interest rates up or down? Then: given that backdrop, which sectors should do well? Finally, within a favoured sector, which specific companies look strongest. The direction of travel is economy → sector → company.

Bottom-up analysis flips the arrow. It starts with an individual company — its earnings, its competitive edge, the quality of its management — and judges the business largely on its own merits. The wider economy and sector come into the picture last, mostly as a sanity check. The direction is company → sector → economy.

An everyday analogy

Imagine house-hunting in a big city. The top-down buyer first decides which neighbourhood is up-and-coming — good transport, new schools, rising demand — and only then looks at houses within it. The bottom-up buyer falls in love with a specific, beautifully built house and will consider it almost wherever it sits, checking the neighbourhood only afterwards. Same city, same goal, opposite starting points.

Why the distinction matters

The two approaches tend to surface different opportunities and carry different blind spots. A top-down investor might catch a whole sector on the rise — say, a boom in renewable energy driven by new policy — and ride the wave across several companies. A bottom-up investor might unearth one exceptional business hidden inside a dull or unloved industry that the top-down crowd skipped entirely.

Knowing which lens you are using also tells you what you might be missing, which is where the honesty comes in.

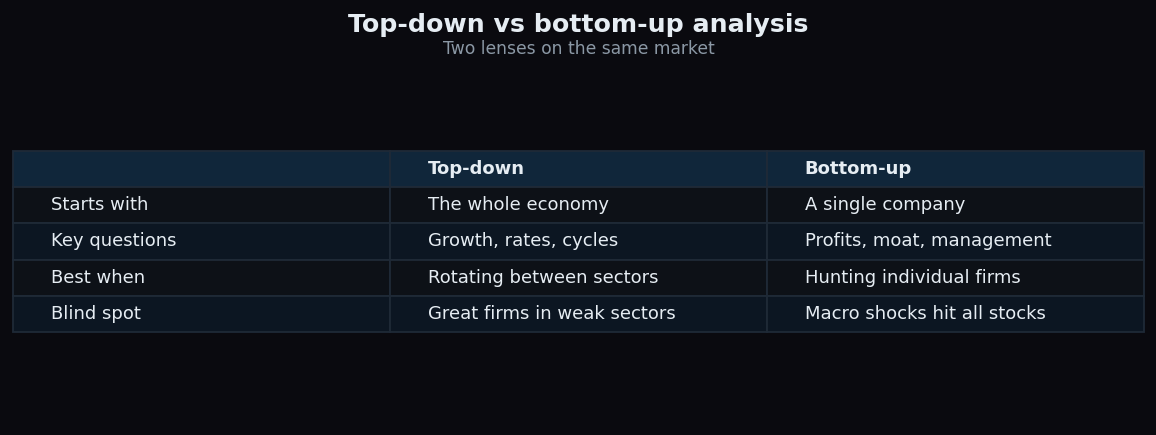

Top-down vs bottom-up at a glance

Laid side by side, the trade-offs are clear:

- Starting point. Top-down begins with the whole economy; bottom-up begins with a single company.

- Key questions. Top-down asks about growth, interest rates and economic cycles. Bottom-up asks about a firm's profits, its moat, and its management.

- Best when. Top-down suits rotating between sectors as conditions change. Bottom-up suits hunting for individual, well-run businesses.

- Blind spot. Top-down can overlook a superb company sitting in a weak sector. Bottom-up can be blindsided by a macro shock — a rate rise or recession — that drags down even excellent firms.

A worked example

Meet two fictional analysts studying the same market. Priya works top-down. She notices interest rates are falling and reasons that home buying will pick up, so housing-related sectors should benefit. She narrows to building materials and then to a cement maker, Ironclad. Her path: economy → sector → company.

Ravi works bottom-up. He stumbles on a small, superbly managed paints company, Zephyr Coatings, with rising profits and loyal customers, and studies it in depth — almost regardless of the sector it sits in. His path: company → sector → economy.

Now watch the two lenses meet. Priya loves the cement sector but must still check that Ironclad itself is well run — a bottom-up question. Ravi loves the Zephyr company but must still check that a slowing economy will not crush paint demand — a top-down question. Each analyst, to be thorough, ends up borrowing the other's lens. That is the real lesson.

Using both together

In practice, most careful research is a blend. A common pattern is to use top-down thinking to decide where to look — which sectors deserve attention given the economic weather — and then bottom-up work to decide which company within that area is genuinely strong. The macro view narrows the field; the company view picks within it. Running both reduces the chance of the classic mistakes: buying a mediocre company just because its sector is hot, or buying a wonderful company straight into an economic storm.

The honest catch

Both methods have real limits, and neither is a shortcut to certainty:

- Top-down leans on forecasting the economy — notoriously hard. Even professionals regularly misjudge the direction of growth, inflation and rates, and a wrong macro call sinks everything built on top of it.

- Bottom-up can ignore the weather. A brilliant company is still exposed to recessions, currency swings and policy shifts. Falling in love with the business can mean underrating the storm around it.

- Both take real work. Neither is a formula. Each demands reading, judgement, and comfort with being uncertain.

- Style is not destiny. A disciplined process matters more than which end you start from. The label is just a description of your route, not a guarantee of the outcome.

So treat top-down and bottom-up as complementary habits of mind rather than rival teams. The most useful question is not "which one is better?" but "which lens am I using right now, and what is it hiding?"

Want to see the macro backdrop and individual-company signals in one place, explained in plain language? TrueTrend's education and market tools help you toggle between both views with confidence. Start free and build the habit.

Key takeaways

- Top-down analysis moves economy → sector → company; bottom-up moves company → sector → economy.

- Top-down asks about growth, rates and cycles; bottom-up asks about a firm's profits, moat and management.

- Top-down can miss a great company in a weak sector; bottom-up can be caught out by a macro shock.

- Most thorough research blends the two: macro to decide where to look, company analysis to decide what to pick.

- Economic forecasting is hard, and a great business can still face a bad economy — both lenses have limits.

- A disciplined process matters more than which end you start from.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.