USD/INR and the Stock Market: How the Rupee Moves Shares

Every day, one number quietly sits behind India's markets: how many rupees it takes to buy one US dollar. That is USD/INR, the rupee-dollar exchange rate. It rarely makes dramatic front-page moves, yet it touches almost everything — the price of your fuel, the profits of software exporters, and whether foreign money is flowing in or leaking out.

This guide explains what USD/INR really means, why a weaker or stronger rupee helps some companies and hurts others, how it ties to foreign flows, and where the simple story gets complicated.

What USD/INR actually tells you

An exchange rate is just the price of one currency in terms of another. If USD/INR is 83, one dollar costs 83 rupees. The confusing part is the direction:

- When USD/INR goes up (say 83 → 85), each dollar costs more rupees — that means the rupee is weaker (this is called depreciation).

- When USD/INR goes down (say 83 → 81), each dollar costs fewer rupees — the rupee is stronger (appreciation).

An easy way to keep it straight: the number is the price of a dollar. A higher price for dollars means a cheaper rupee.

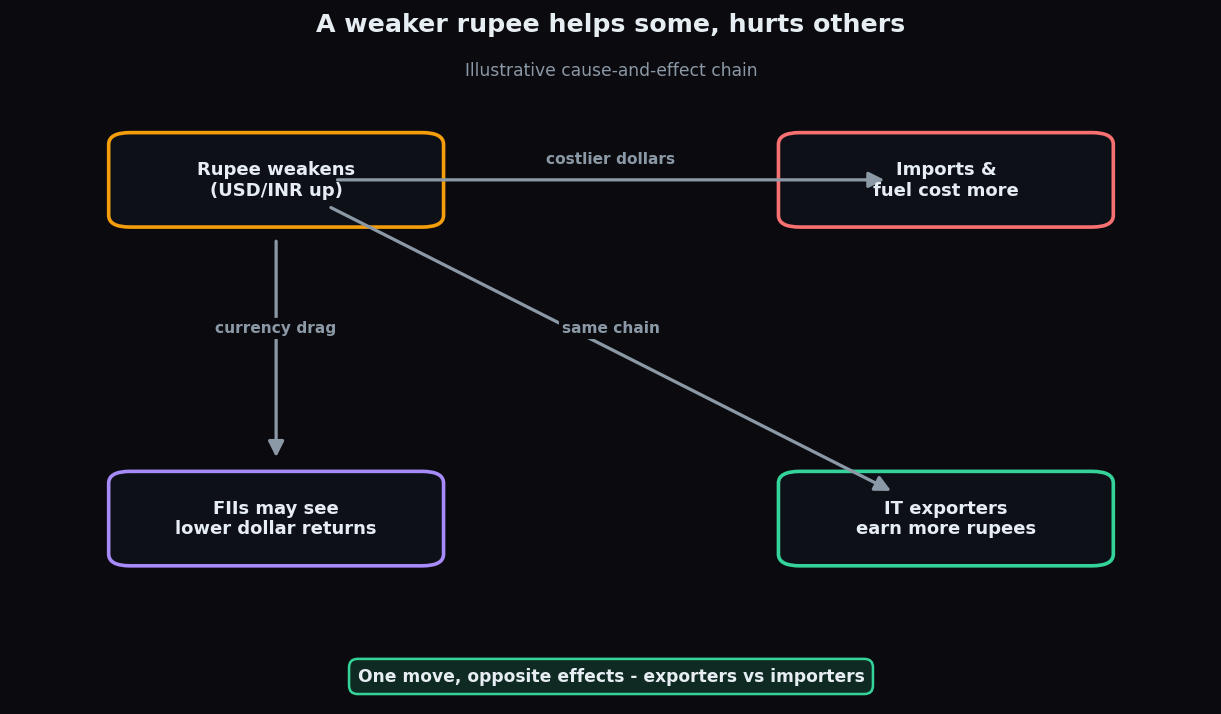

Why a weaker rupee is a two-sided coin

Currency moves do not lift or sink the whole market evenly. They redistribute. The same weaker rupee helps one set of companies and hurts another.

The exporters (helped by a weaker rupee)

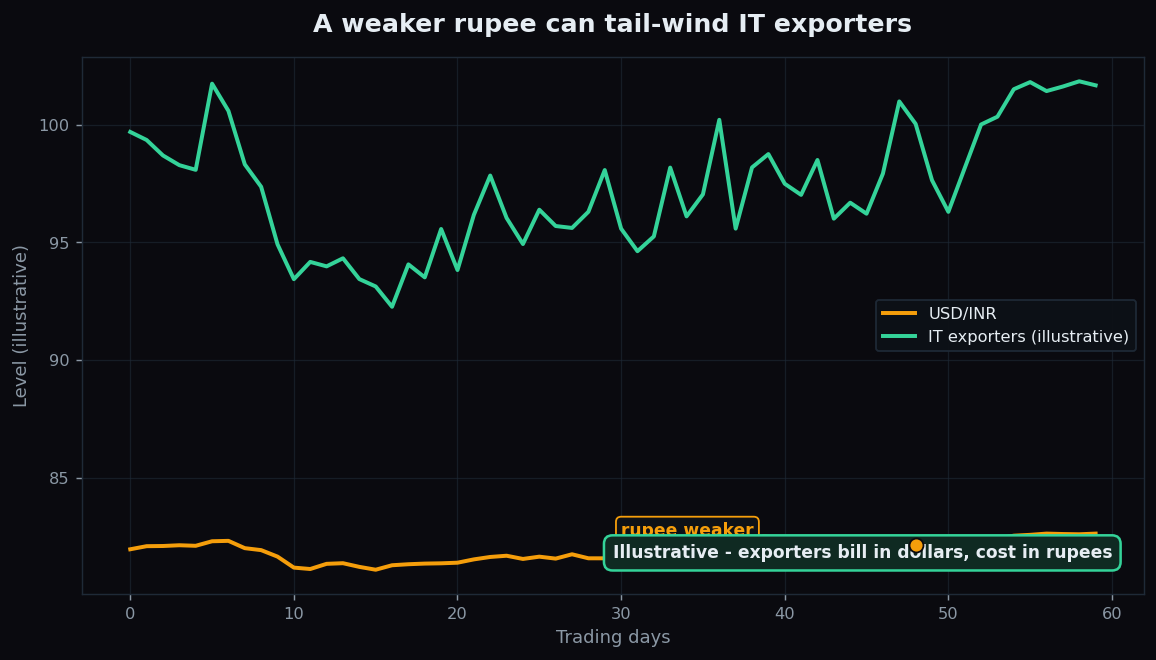

An exporter sells abroad and gets paid in dollars, but pays most of its costs (salaries, offices) in rupees. When the rupee weakens, each dollar of revenue converts into more rupees, while costs barely change. India's IT services and pharma exporters are the classic examples. A weaker rupee is a tailwind for their reported profits.

The importers (hurt by a weaker rupee)

An importer buys from abroad in dollars but sells at home in rupees. When the rupee weakens, those dollar purchases cost more rupees, squeezing margins. Think oil marketers, firms that import machinery or electronics components, and companies with large dollar-denominated debt (their repayments get heavier).

A worked example (illustrative numbers)

Imagine a software firm bills a US client $1 million for a project.

- At USD/INR of 80, that is ₹8.0 crore in revenue.

- If the rupee weakens to 84, the same $1 million becomes ₹8.4 crore — an extra ₹40 lakh, with no extra work.

Now flip it. A company importing $1 million of components pays ₹8.0 crore at 80, but ₹8.4 crore at 84 — ₹40 lakh more for the same goods. One currency move, opposite outcomes. (Round numbers, purely to show the mechanics.)

The FII flow connection

Currency also drives foreign money. FIIs (Foreign Institutional Investors — overseas funds) invest in Indian shares but ultimately measure their returns in dollars. Suppose an FII buys Indian stocks and the market rises 5% in rupees — but the rupee weakens 4% over the same period. In dollar terms, most of that gain is eaten away by the currency.

So a fast-weakening rupee can make India less attractive to foreign funds, sometimes triggering outflows — which can weaken the rupee further. A stable or strengthening rupee does the opposite, supporting inflows. This is why currency and foreign flows are often watched together as one story.

The honest catch

The textbook logic — weak rupee helps exporters, hurts importers — is a starting point, not a law. Real companies hedge their currency exposure (locking in rates in advance), so the effect is often muffled or delayed. A firm might export and import heavily, netting out the impact. And a rupee move driven by a global dollar surge feels very different from one driven by a local problem, even at the same exchange rate. Currencies are also famously hard to predict; even seasoned desks get direction wrong.

Read USD/INR as important context for which parts of the market have a tailwind or headwind — not as a dial that moves everything the same way.

The rupee, foreign flows, and the sectors they touch move as one connected system. TrueTrend pulls these currency and flow cues into a single plain-English daily read, so you can see the macro backdrop without stitching it together from ten tabs. Create a free account to follow the setup.

Key takeaways

- USD/INR is the price of a dollar in rupees. A higher number means a weaker rupee.

- A weaker rupee tends to help exporters (IT, pharma) and hurt importers and dollar-debt holders.

- FIIs measure returns in dollars, so a fast-weakening rupee can discourage foreign inflows.

- Currency and foreign flows are best watched together as one story.

- Hedging, mixed business models, and the reason behind a move all soften the textbook effect.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.