What Are Derivatives? A Complete Beginner's Guide

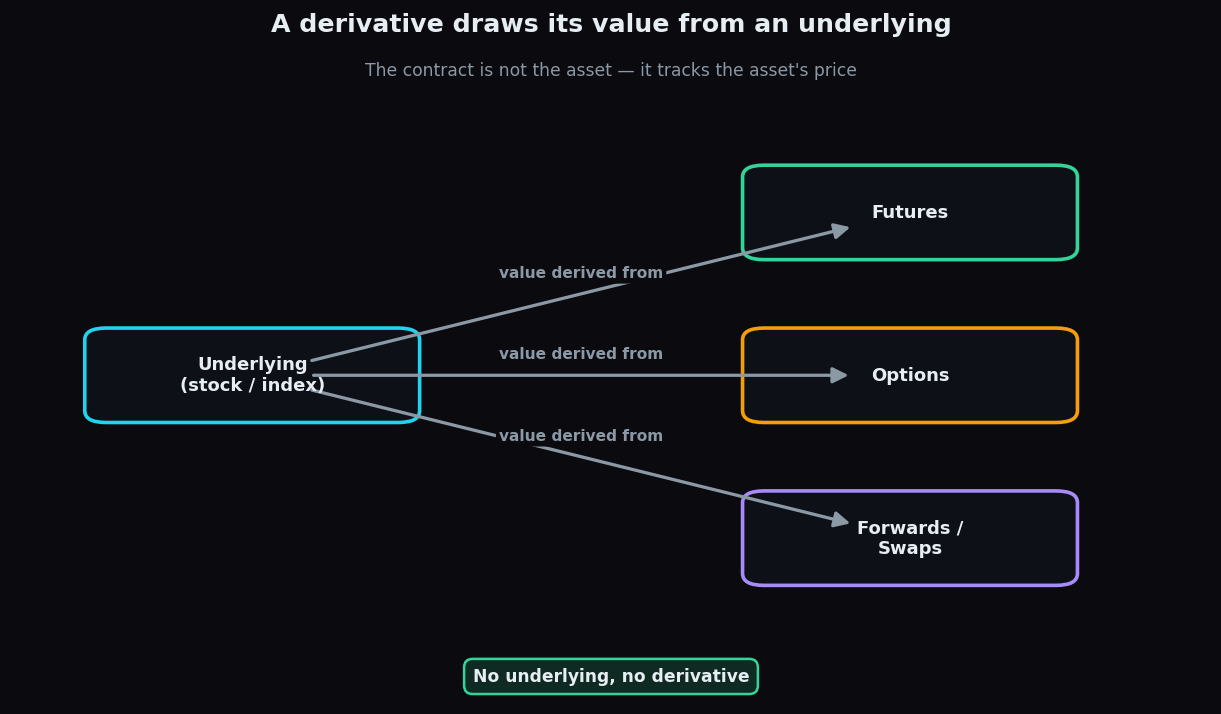

A derivative is a financial contract whose value comes from something else — a stock, an index, a currency, or a commodity. The contract itself has no value of its own. It simply tracks the price of that other thing, which traders call the underlying. If you have ever bought a gift voucher whose worth depends entirely on the shop it belongs to, you already understand the core idea: the paper is just a claim, and its value is borrowed from somewhere else.

What exactly is a derivative?

The word sounds intimidating, but it is literal. The contract's value is derived from an underlying asset. Buy a contract linked to the Nifty 50 index, and its price rises and falls with the index. The contract is a promise about a price, a quantity, and a date — not the asset itself.

Think of it like a deposit on a house. You agree today on a price for a future purchase. You do not own the house yet, but your agreement already has value: if house prices jump before the sale completes, your right to buy at the old price is suddenly worth a lot. The agreement — the derivative — moves in value because the house — the underlying — moved.

Why derivatives exist

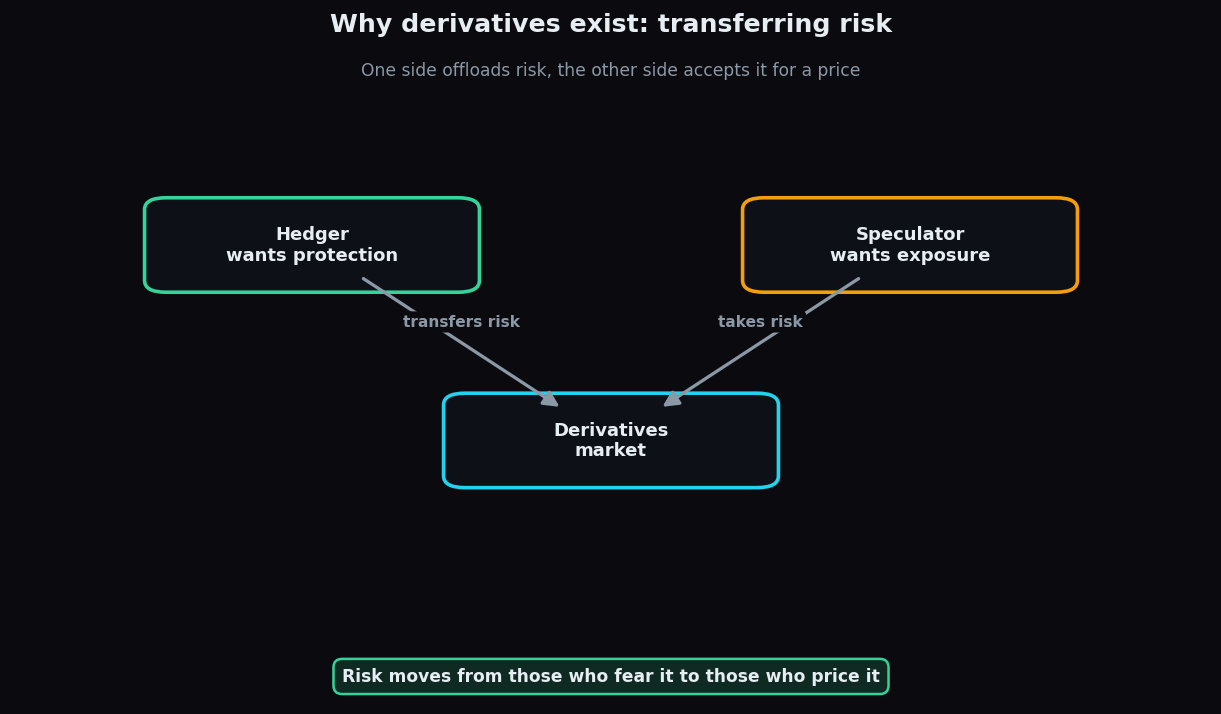

Derivatives were not invented to make trading exciting. They exist to solve a real, old problem: moving risk from people who do not want it to people who are willing to carry it. There are two broad groups who meet in this market.

The first group is hedgers. A hedger already faces a price risk and wants protection. Picture a farmer who will harvest wheat in three months. He does not know what wheat will sell for then. By locking a price today through a derivative, he removes that uncertainty. An airline worried about fuel costs, or a fund manager worried about a market fall, hedges for the same reason — to make tomorrow more predictable.

The second group is speculators. A speculator has no underlying risk to protect. They willingly take on risk because they have a view on where prices are heading and want to profit if they are right. Speculators are often painted as villains, but they play a useful role: they provide the other side of the hedger's trade, and their constant buying and selling keeps the market liquid — meaning you can usually find someone to trade with quickly.

So the market is a meeting place. One side pays to shed risk; the other side accepts risk hoping to be paid for it. That transfer is the entire economic point of a derivative.

The main types of derivatives

Most derivatives fall into four families. They share the same DNA — a value tied to an underlying — but differ in their rules.

1. Futures

A futures contract is an obligation to buy or sell the underlying at a set price on a set future date. Both sides are bound: the buyer must buy, the seller must sell. Futures are standardised and trade on an exchange, so they are easy to enter and exit. Because they are an obligation in both directions, gains and losses are symmetric.

2. Options

An option gives the buyer a right, not an obligation. A call option is the right to buy at a fixed price; a put option is the right to sell at a fixed price. The buyer pays a fee — the premium — for this right and can simply walk away if the deal turns sour. That one-sided flexibility is what makes options so different from futures.

3. Forwards

A forward is a close cousin of a future: also an agreement to trade at a set price on a future date. The difference is that forwards are private, customised deals between two parties, not standardised exchange products. That flexibility comes with extra risk that the other side might not honour the deal.

4. Swaps

A swap is an agreement to exchange one stream of payments for another — for example, swapping a floating interest rate for a fixed one. Swaps are mostly used by large institutions to manage interest-rate or currency exposure, and they rarely concern a beginner directly.

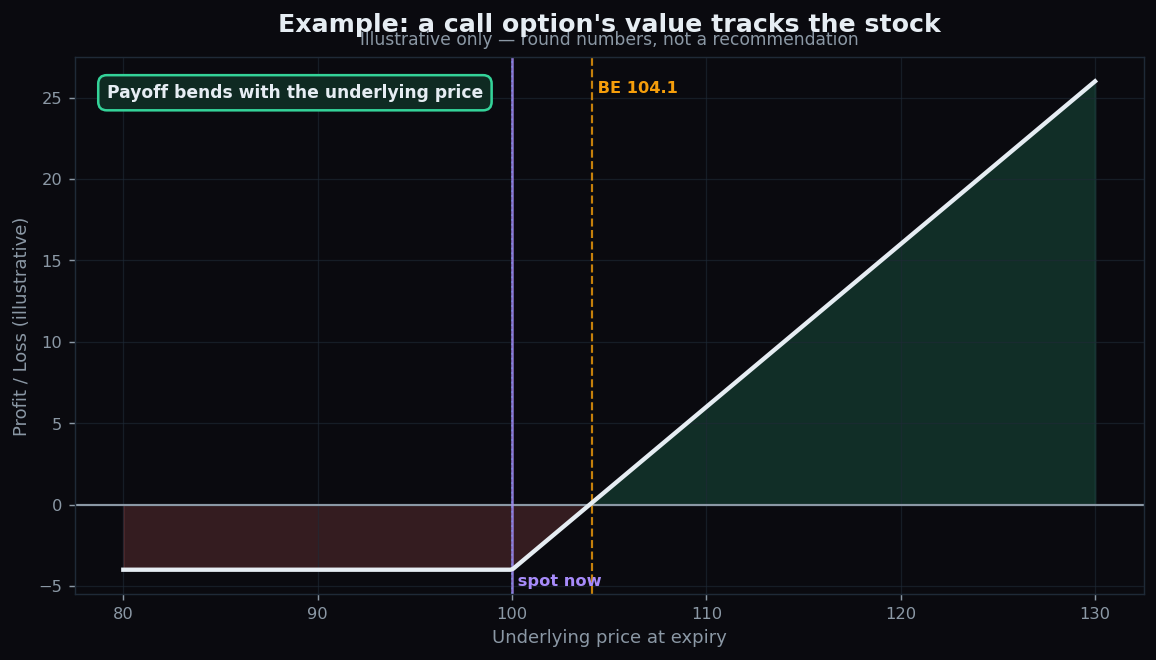

A simple worked example

Suppose a stock trades at 100 today. You believe it will rise but you do not want to spend 100 per share. Instead you buy a call option with a strike price of 100 — the fixed price at which you may buy — for a premium of 4.

- If the stock climbs to 110, your right to buy at 100 is worth 10. Subtract the 4 you paid, and your gain is 6 per share.

- If the stock falls to 90, you simply do not use the option. You lose only the 4 premium — nothing more.

That asymmetry — small fixed cost, larger potential payoff — is what draws people to options. It is also why options are priced carefully, because that flexibility is not free. This is an illustration of how the mechanics work, not a suggestion to trade.

The honest catch

Derivatives are powerful precisely because they offer leverage — control over a large position for a small outlay. Leverage cuts both ways. A modest move in the underlying can produce an outsized gain, but an equally modest move the wrong way can wipe out your stake just as fast. Futures can even lose more than your initial margin because the obligation is binding.

Derivatives also expire. Unlike a share you can hold for years, most derivatives have a deadline, and time itself erodes the value of options. And the pricing involves moving parts — volatility, time, interest rates — that beginners routinely underestimate. The tool is neutral; the danger lives in using it without understanding it.

Understanding how derivatives move before risking money is the cheapest lesson you will ever buy. TrueTrend turns live market structure into plain-language context so you can learn how these instruments behave. Create a free account to start exploring.

Key takeaways

- A derivative has no value of its own — it borrows value from an underlying asset.

- Derivatives exist to transfer risk: hedgers shed it, speculators accept it for potential reward.

- The four main types are futures and forwards (obligations), options (a right, not an obligation), and swaps (exchanging payment streams).

- Leverage is the headline feature and the headline danger — it amplifies gains and losses alike.

- Derivatives expire, and their pricing depends on time and volatility, not just direction.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.