What Is Hedging? Protecting a Portfolio

Imagine you own something valuable and you are worried it might lose value next month — but you do not want to sell it. Is there a way to protect it without giving it up? In the markets, yes: it is called hedging. Hedging is one of the oldest and most sensible uses of the derivatives market, and yet it is widely misunderstood as either a magic shield or a waste of money. It is neither. It is insurance — with all the trade-offs that insurance implies.

What hedging is

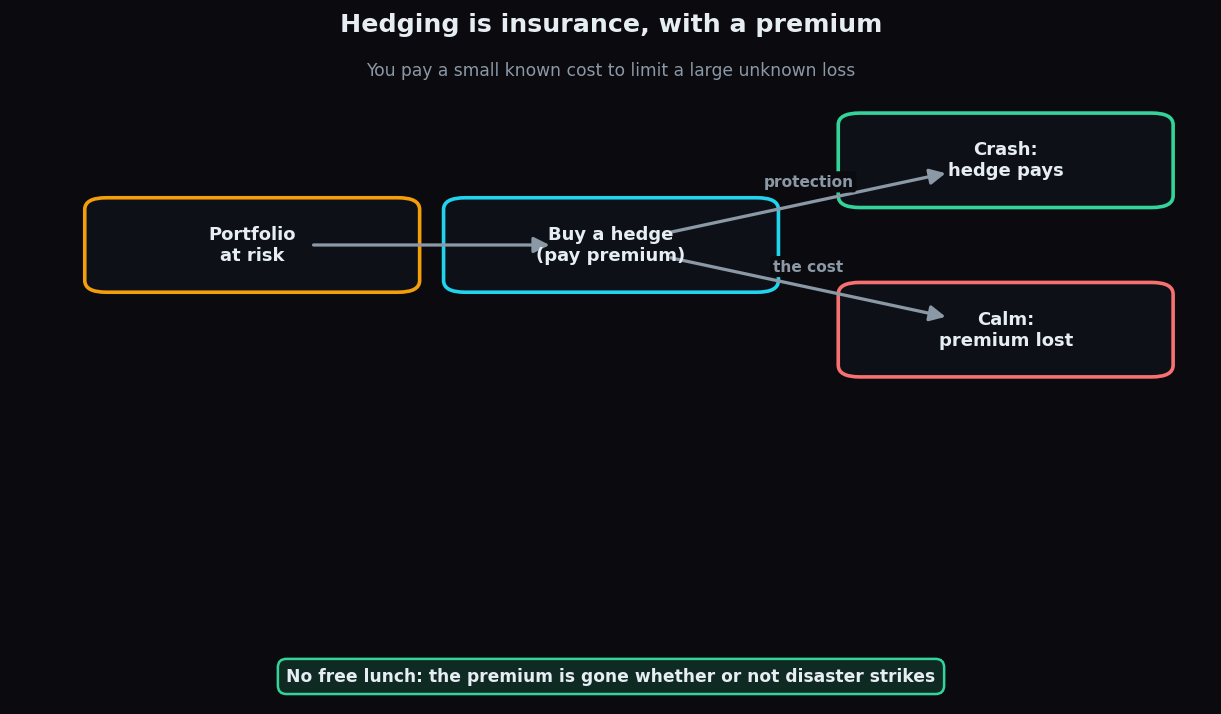

A hedge is a second position taken specifically to offset the risk of an existing one. You are not trying to make money on the hedge itself. You are trying to reduce the damage if your main holding moves against you. If your first position loses, the hedge is designed to gain, softening the blow.

The cleanest analogy is car insurance. You pay a premium every year. In most years nothing happens and that premium is simply gone — you got no accident and no payout. But in the one year you have a crash, the insurance absorbs a loss that could have been ruinous. You did not buy insurance hoping to profit. You bought it so a bad event would not wreck you. A hedge is exactly that logic applied to a portfolio.

How a hedge is built

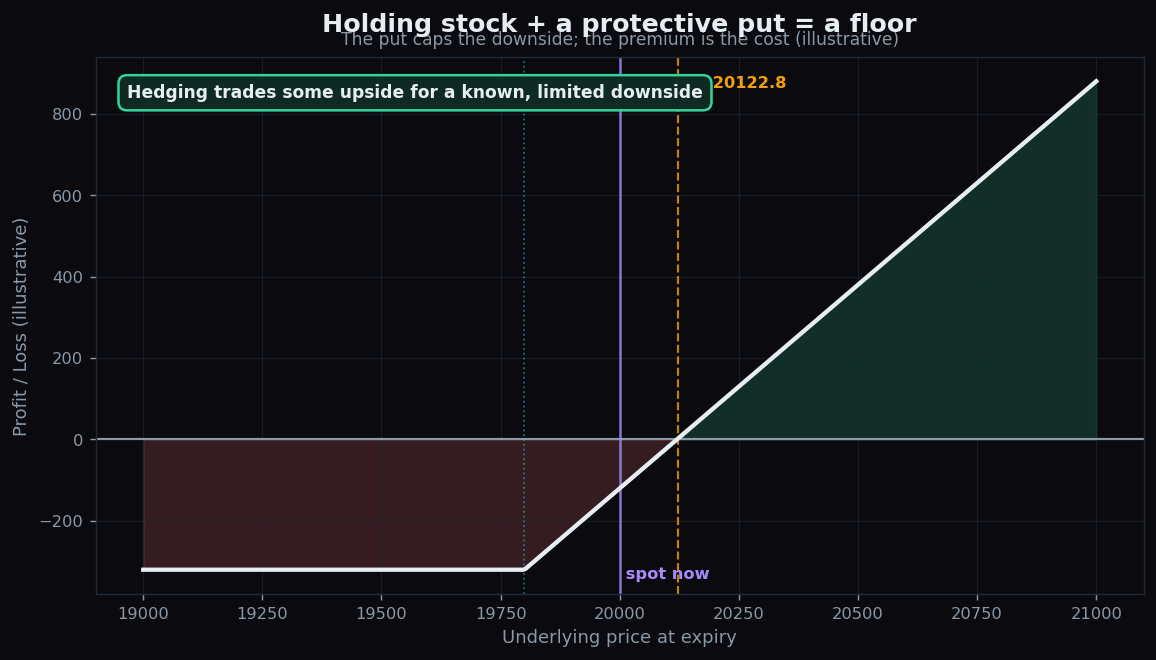

A classic beginner-friendly hedge is the protective put. You hold an asset — say a basket of shares tracking an index — and you buy a put option, which gives you the right to sell at a fixed strike price. If the market crashes, the put gains value and offsets your falling shares. If the market rises, you let the put expire and simply lose its premium, the fee you paid. The picture below shows how the two combine into a payoff with a floor.

Look at the left side of that chart: instead of falling forever, the combined line flattens out. That flat portion is your protection — the most you can lose is capped. The cost of drawing that floor is the premium you paid, which is why the whole line sits a little lower than holding the asset alone.

Why hedging matters

Hedging matters because it lets you stay invested through uncertainty instead of panic-selling. A farmer who locks in a crop price before harvest can plan calmly regardless of what prices do. An investor holding a portfolio into a nervous event — an election, a big data release — can cap the downside without dumping good long-term holdings and triggering taxes and regret. Hedging converts a scary unknown loss into a known, bounded cost. For many people, that predictability is worth paying for.

A worked example with round numbers

Say you hold a portfolio worth 20,000 per unit and you buy a protective put at a strike of 19,800 for a premium of 120. These are illustrative figures, not advice.

- Market crashes to 19,000: your holding falls 1,000, but the put lets you sell at 19,800, so your effective floor is 19,800 minus the 120 premium, about 19,680. The crash below that point does not touch you.

- Market rises to 20,600: the put expires worthless. You lose the 120 premium, but your holding gained 600, for a net gain of about 480. You still profited — just slightly less than if you had skipped the hedge.

- Market barely moves: the put expires worthless and the 120 premium is simply gone — the cost of protection you did not end up needing.

The honest catch: the cost and the trade-off

Here is where beginners get surprised. Hedging is not free, and it is not free money either.

- You pay a premium whether or not disaster strikes. Like insurance, most of the time the hedge expires unused and the premium is a pure cost. Hedge constantly and those premiums quietly drag on returns.

- You give up some upside. The premium comes out of your gains, so a hedged portfolio climbs a little slower in good times. Protection is bought with performance.

- A hedge is not a guarantee. The offset is rarely perfect. The instrument you hedge with may not track your holding exactly, and options carry their own time decay. And note the mirror image: whoever sold you that put took on large, open-ended risk in exchange for the premium — the risk did not vanish, it moved to someone else. There is no free lunch anywhere in this trade.

So hedging is a deliberate exchange: you accept a small, known cost today to remove a large, unknown loss tomorrow. Whether that exchange is worthwhile depends entirely on how much the downside would hurt you — a question only you can answer.

Good risk decisions start with seeing your exposure clearly. TrueTrend turns live market structure into plain-English context so you can study how positions interact. Create a free account to learn more.

Key takeaways

- Hedging is a second position taken to offset the risk of an existing one — insurance, not a profit centre.

- A protective put puts a floor under a holding: the downside is capped, the upside continues, minus the premium.

- Hedging converts an unknown potential loss into a known, bounded cost — useful for staying invested through uncertainty.

- The premium is paid whether or not trouble arrives, and it trims your gains in good times.

- No hedge is a guarantee, and the risk you shed is simply transferred to the seller — there is no free lunch.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.