DCF Valuation Explained for Beginners, Step by Step

Ask a professional analyst how they decide what a company is really worth, and many will mention a DCF — a discounted cash flow model. It sounds intimidating, full of spreadsheets and Greek symbols. But the core idea is something a child understands: a rupee in your hand today is worth more than a rupee promised next year. This guide builds DCF valuation from that single simple idea, works through an example with round numbers, and is honest about why the method can be dangerously misleading.

The one idea behind it all: the time value of money

Would you rather receive Rs 100 today or Rs 100 a year from now? Almost everyone picks today — and they are right. Money today can be saved to earn interest, it is certain rather than promised, and inflation slowly eats the value of future rupees. This is called the time value of money: the same amount is worth less the further into the future you must wait for it.

A DCF valuation uses this to answer one question: what are all of a company's expected future cash flows worth in today's money? Add those present-day values together and you get an estimate of what the whole business — and each share — is worth right now.

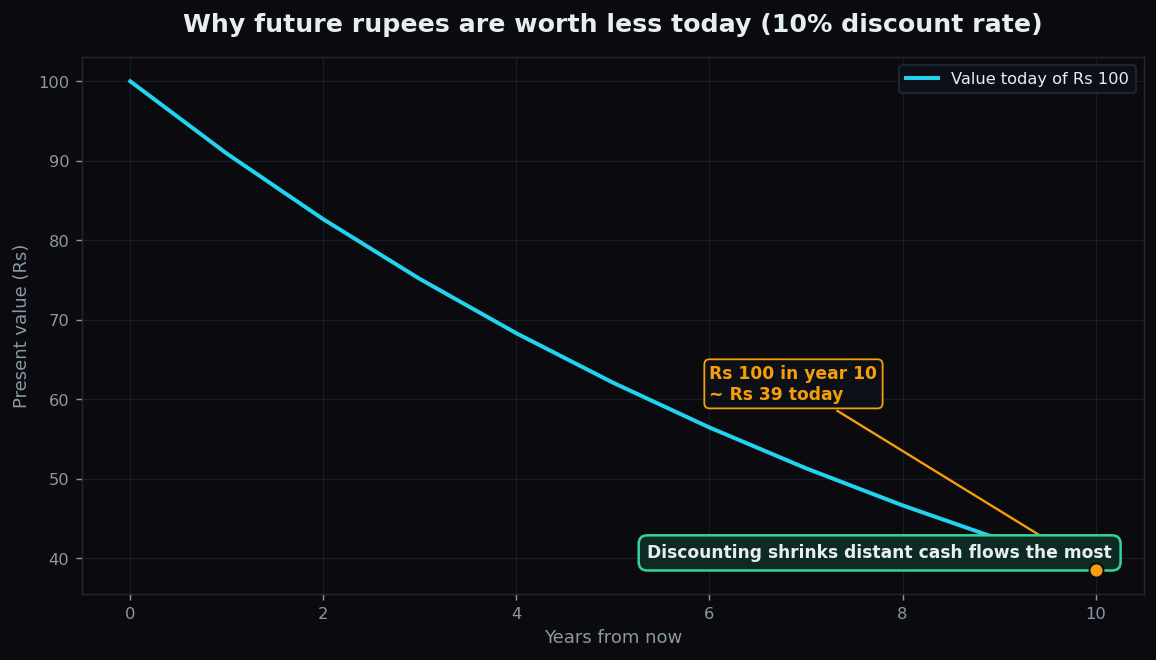

Discounting: shrinking future cash to today's value

Discounting is the tool that converts a future rupee into today's rupee. You pick a yearly rate — the discount rate — that reflects both the return you expect and the risk that the cash may not arrive. Each year further out gets shrunk more.

Using a 10% discount rate, Rs 100 promised in various future years is worth this much today:

- In 1 year: about Rs 91

- In 5 years: about Rs 62

- In 10 years: about Rs 39

The curve falls away steadily — distant cash is shrunk the most. That single behaviour is the beating heart of every DCF model.

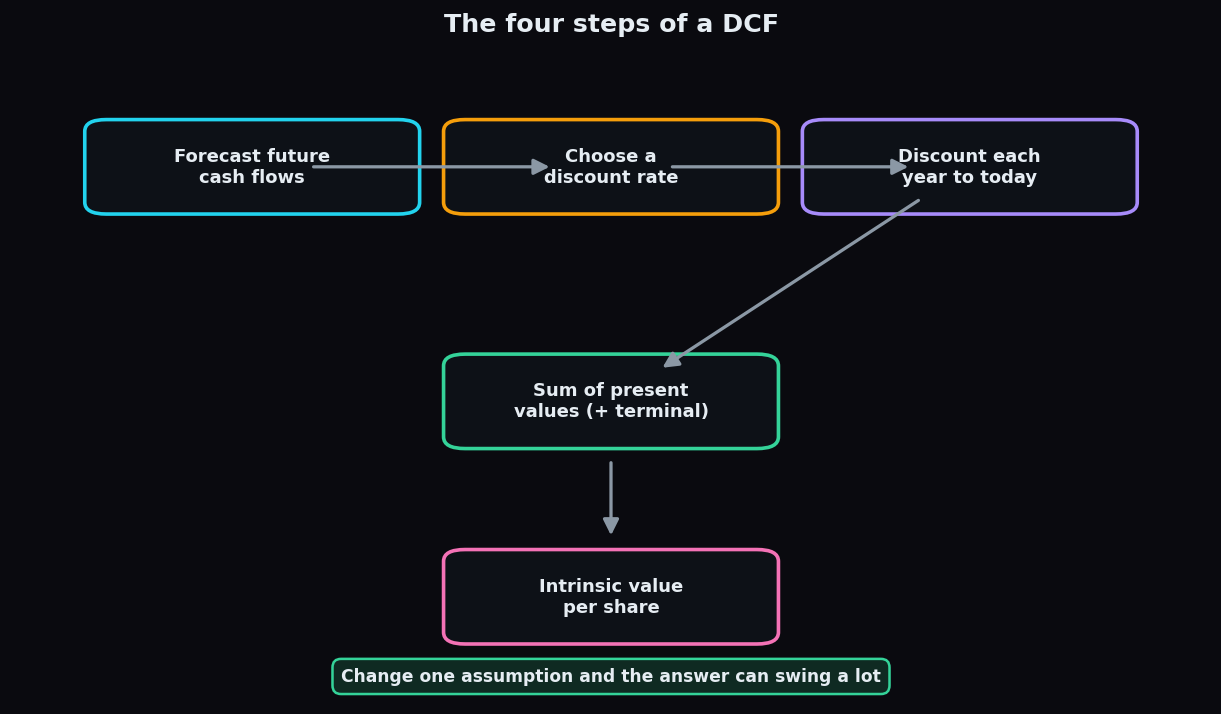

The four steps of a DCF

Every DCF, however fancy, follows the same four steps:

- Forecast future cash flows. Estimate the free cash the business will generate each year for, say, the next five to ten years.

- Choose a discount rate. Pick the yearly rate used to shrink those future flows, reflecting risk and expected return.

- Discount each year to today. Convert every future year's cash into present-day value.

- Add them up. Sum the present values (plus a "terminal value" for the years beyond the forecast) to get the estimated worth of the business, then divide by the number of shares.

A simplified worked example

Take a fictional software firm, Nimbus Systems. Suppose we expect it to produce free cash flow of Rs 100 crore every year for three years, and we use a 10% discount rate. Discount each year:

- Year 1: 100 ÷ 1.10 = Rs 91 crore

- Year 2: 100 ÷ 1.21 = Rs 83 crore

- Year 3: 100 ÷ 1.33 = Rs 75 crore

Add the present values: 91 + 83 + 75 = Rs 249 crore. So even though the company will hand over Rs 300 crore in raw cash over three years, that stream is worth only about Rs 249 crore in today's money. If Nimbus had 10 crore shares, this simplified model implies roughly Rs 25 per share of value from these three years. (A real DCF would also add a terminal value for cash beyond year three.)

Analogy: a DCF is like pricing a fruit tree. You estimate the baskets of fruit it will bear each year, then decide how much a future basket is worth to you today — because a basket ten summers away is far less certain, and less valuable now, than this year's harvest.

The honest catch: garbage in, garbage out

Here is the warning every beginner must hear. A DCF produces one confident-looking number — "the share is worth Rs 25" — but that number is only as good as the guesses fed into it. And it is extremely sensitive to those guesses.

- The growth forecast is a guess. No one truly knows a company's cash flows a decade out. Nudge the assumed growth up a little and the value can jump substantially.

- The discount rate swings everything. Move it from 10% to 12% and every future rupee shrinks faster, pulling the valuation down noticeably. There is no single "correct" discount rate.

- The terminal value dominates. In many models, most of the total value comes from the terminal value — the murkiest, most assumption-heavy part.

- Precision is an illusion. A DCF can output "Rs 25.37" and feel scientific, yet reasonable people using slightly different assumptions might get Rs 18 or Rs 34.

Because of this sensitivity, careful analysts never trust a single DCF number. They run a range of assumptions to see how wide the outcome gets, and they treat the result as a rough guide rather than a precise price tag. A DCF is a way to organise your thinking about value — not a crystal ball. It pairs well with sturdier, cash-based checks like whether the business actually generates free cash flow in the first place.

Valuation models describe what a business might be worth; live market structure shows how its stock is actually trading. TrueTrend turns raw market data into plain-English context so beginners can learn the mechanics calmly. Start free to explore.

Key takeaways

- A DCF values a company by estimating its future cash flows and converting them to today's money.

- The core idea is the time value of money: future rupees are worth less than rupees today.

- Discounting shrinks each future year's cash — at 10%, Rs 100 in ten years is worth about Rs 39 today.

- The four steps: forecast cash flows, choose a discount rate, discount each year, then sum to a value per share.

- DCF is highly sensitive to its assumptions; treat the output as a range and a thinking tool, never a precise answer.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.