Intrinsic Value and Time Value of Options Explained

Every option premium is made of exactly two ingredients: intrinsic value and time value. Learn to split any premium into these two parts and you gain a kind of X-ray vision — you can suddenly see how much of the price is solid, real worth and how much is fragile possibility that fades a little every single day. This single skill quietly separates beginners who guess from those who understand what they are holding.

The two halves of every premium

The rule is simple and never breaks: premium = intrinsic value + time value. Whatever an option costs, you can always carve it into these two pieces. They behave very differently, which is exactly why it pays to tell them apart.

Intrinsic value is the part backed by reality — the gain you would pocket if you exercised the option right now. Time value is the rest — the premium you pay purely for the chance that the price keeps moving your way before the option expires. One is concrete; the other is hope with a price tag.

Calculating intrinsic value

Intrinsic value answers a blunt question: if I exercised this option this second, how much would it be worth? For a call (the right to buy), it is the current price minus the strike. For a put (the right to sell), it is the strike minus the current price. And it can never fall below zero — if exercising would lose money, you would not do it, so the floor is zero.

Take a call with a strike of 100 when the stock trades at 108. Intrinsic value = 108 − 100 = 8. That 8 is genuine, bankable worth. If the same stock were at 95, the call would have zero intrinsic value — it would be out-of-the-money, with exercising at 100 making no sense when you could buy at 95 in the open market.

Calculating time value

Once you know intrinsic value, time value is whatever is left over: time value = premium − intrinsic value. If that 100-strike call costs 12 while the stock is at 108, then time value = 12 − 8 = 4.

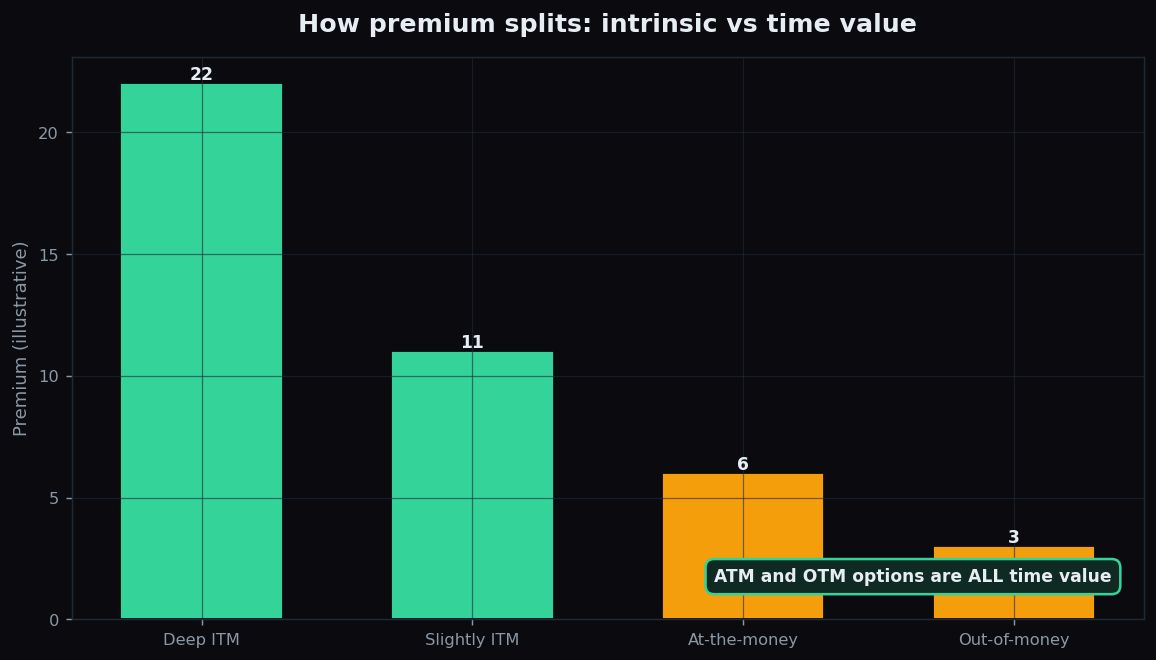

Here is the part that surprises newcomers. An at-the-money or out-of-the-money option has zero intrinsic value, which means its entire premium is time value. Buy an out-of-the-money option and you are paying 100% for possibility — there is no solid floor underneath the price at all.

The deeper in-the-money an option is, the more of its premium is solid intrinsic value and the less is fragile time value. Move toward at-the-money and out-of-the-money, and the balance tips entirely toward time value. That is why far out-of-the-money options look cheap — they are pure hope, and hope is the first thing to evaporate.

Time value decays to zero

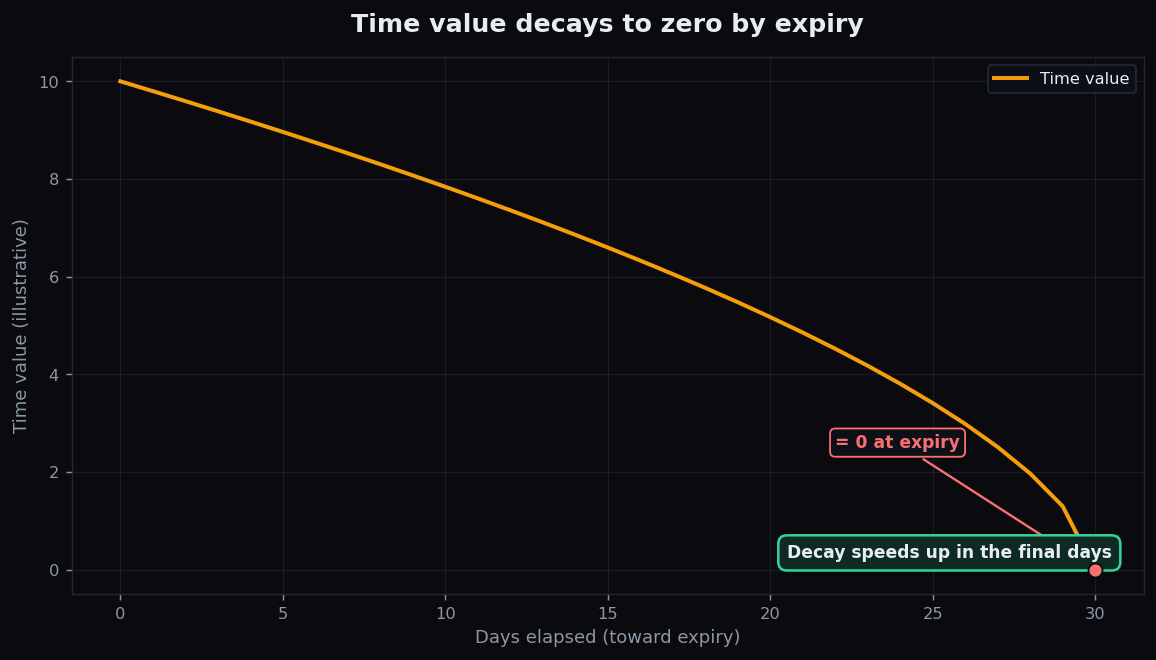

The defining feature of time value is that it is on a countdown. With every day that passes, there is less time for the price to move, so the time-value portion shrinks. By the moment of expiry, time value reaches exactly zero. At expiry, an option is worth only its intrinsic value — nothing more.

This erosion is called time decay, and it does not happen evenly. Early on, the drip is slow. In the final days before expiry, it accelerates sharply — the curve falls off a cliff. An out-of-the-money option that is all time value can lose a large chunk of its worth in the last week even if the underlying barely moves. Think of it like an ice cube: it melts slowly in the cold, then faster and faster as the room warms, until nothing is left.

A worked example over time

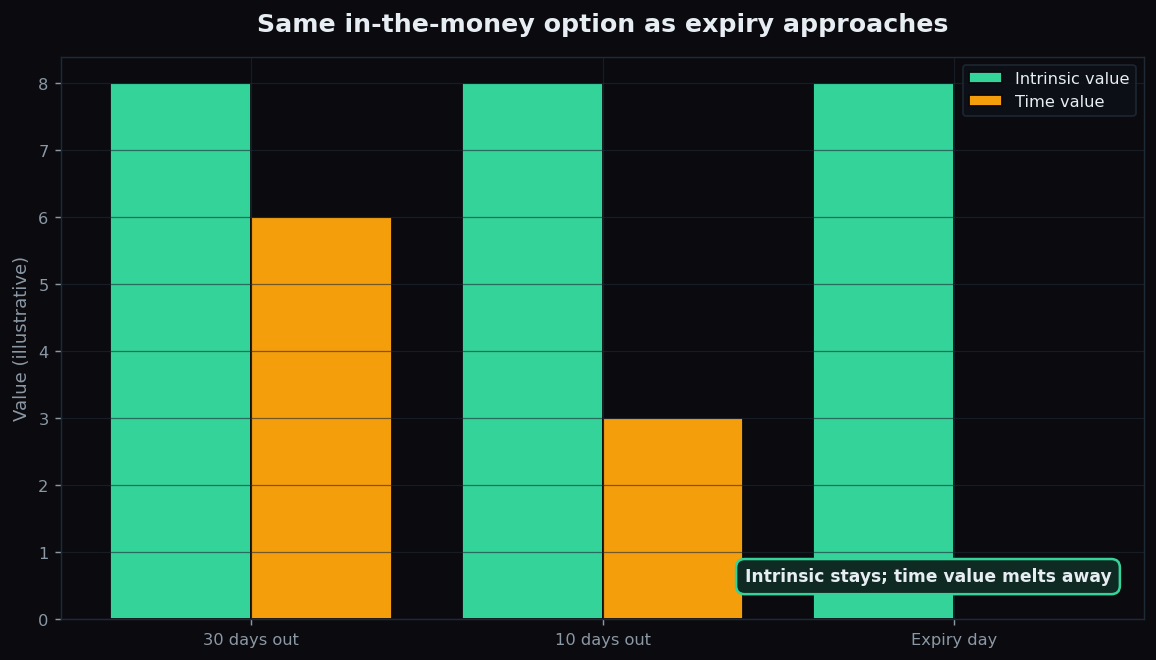

Hold one in-the-money call as expiry approaches. Say it carries a steady 8 of intrinsic value the whole way (the stock holds at 108), and we watch its time value shrink:

- 30 days out: intrinsic 8 + time value 6 = premium 14.

- 10 days out: intrinsic 8 + time value 3 = premium 11.

- Expiry day: intrinsic 8 + time value 0 = premium 8.

The intrinsic value never budged, yet the premium fell from 14 to 8 — a loss of 6 — purely from time decay, with no move against you at all. This is the quiet tax every option holder pays for the privilege of holding. These are illustrative round numbers, not a recommendation to trade.

The honest catch

Time decay is the reason an option buyer can be completely right about direction and still lose money. If you pay mostly for time value and the move you expected arrives too slowly — or not at all — that time value drains away and your option is worth less, or nothing. The clock is always running, and it runs against the buyer.

The flip side is that time decay helps the option seller, who collects the premium and benefits as time value melts. Neither side is free: the buyer pays for possibility, the seller is paid for risk. Before holding any option, split its premium into intrinsic and time value and ask honestly how much of what you are paying is real worth and how much is a melting ice cube. Volatility complicates this further — calmer-than-expected markets shrink time value too — as our explainer on the expected move baked into option prices shows.

Seeing the two halves of a premium clearly is what turns option trading from a gamble into a studied craft. TrueTrend translates live option structure into plain-language context for learners. Create a free account to explore it.

Key takeaways

- Every premium = intrinsic value + time value, and the two behave very differently.

- Intrinsic value is the immediate exercise worth (a call's price minus strike, a put's strike minus price), never below zero.

- Time value is the rest — the price of remaining possibility; at-the-money and out-of-money options are all time value.

- Time decay erodes time value to zero by expiry, accelerating in the final days.

- You can be right on direction and still lose, because time value melts whether or not the price moves.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.