Option Premium: What You Pay and Why It Moves

When you buy an option, you hand over a single number called the premium — the price of the contract. It can feel like a black box: why is one option priced at 12 and another at 3? The answer is surprisingly orderly. Every premium is built from just two parts, and once you can see those parts, option prices stop looking random and start making sense.

What is the premium?

The premium is the amount an option buyer pays an option seller for the contract. It is paid up front, the moment the trade is struck. For the buyer, it is the entire cost of the position and the most that can be lost. For the seller, it is income received in exchange for taking on risk. Think of it as the sticker price of an option.

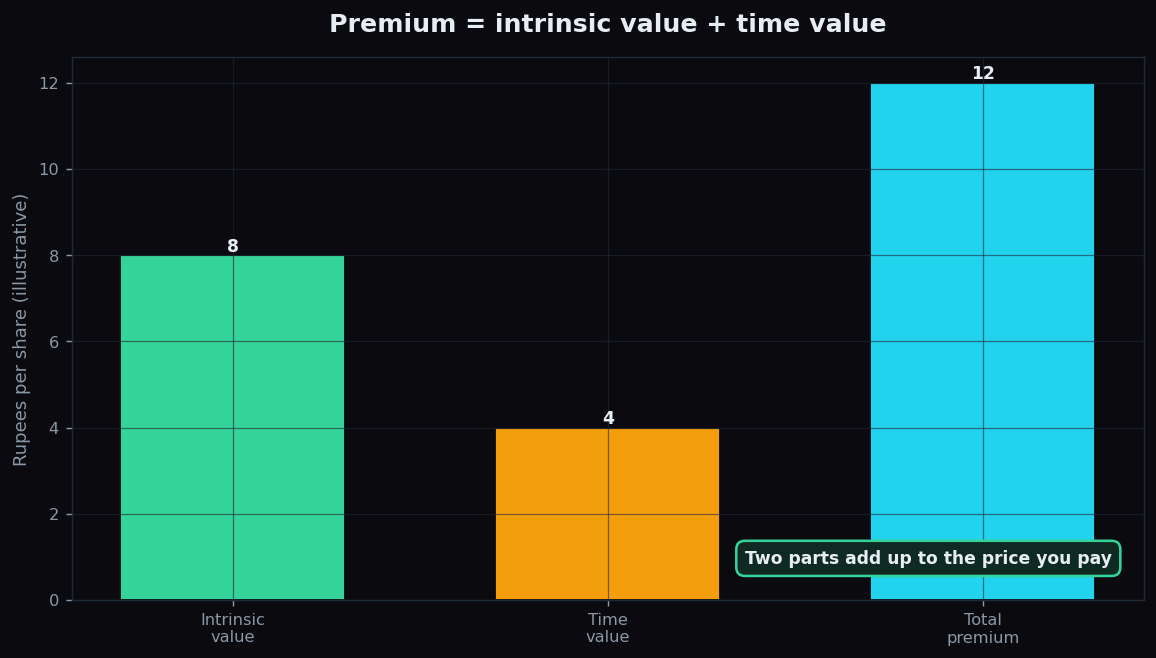

That sticker price is never one solid lump. It always splits cleanly into two pieces: intrinsic value and time value. Premium = intrinsic value + time value. Everything else in this article is just unpacking those two terms.

Part one: intrinsic value

Intrinsic value is the real, here-and-now worth of an option if you exercised it this instant. It is the part of the premium backed by actual gain already sitting on the table.

For a call option, intrinsic value is the current price minus the strike, but never less than zero. If a stock trades at 108 and your call has a strike of 100, the intrinsic value is 108 − 100 = 8. You could buy at 100 and the asset is worth 108, so 8 is locked-in worth.

For a put, it flips: strike minus current price, floored at zero. A put with a strike of 100 when the stock trades at 92 has intrinsic value of 100 − 92 = 8.

Crucially, intrinsic value can never be negative. If exercising would lose money, you simply would not exercise — so the floor is zero. An option with zero intrinsic value is said to be out-of-the-money; its entire premium is made of the second ingredient.

Part two: time value

Time value is everything in the premium beyond intrinsic value. It is the price of possibility — the extra amount buyers willingly pay because the option still has time left for the price to move further in their favour.

Picture two concert tickets that are identical except one is for a show tonight and the other for a show next month. The month-away ticket carries more optionality — more time for plans to change, for the act to get hotter. That extra worth is time value. In options, the more time remaining and the more the market could swing, the larger the time value.

Here is the arithmetic. If a call's premium is 12 and its intrinsic value is 8, then its time value is 12 − 8 = 4. That 4 is what you are paying purely for the chance that the stock climbs even higher before expiry.

A full worked example

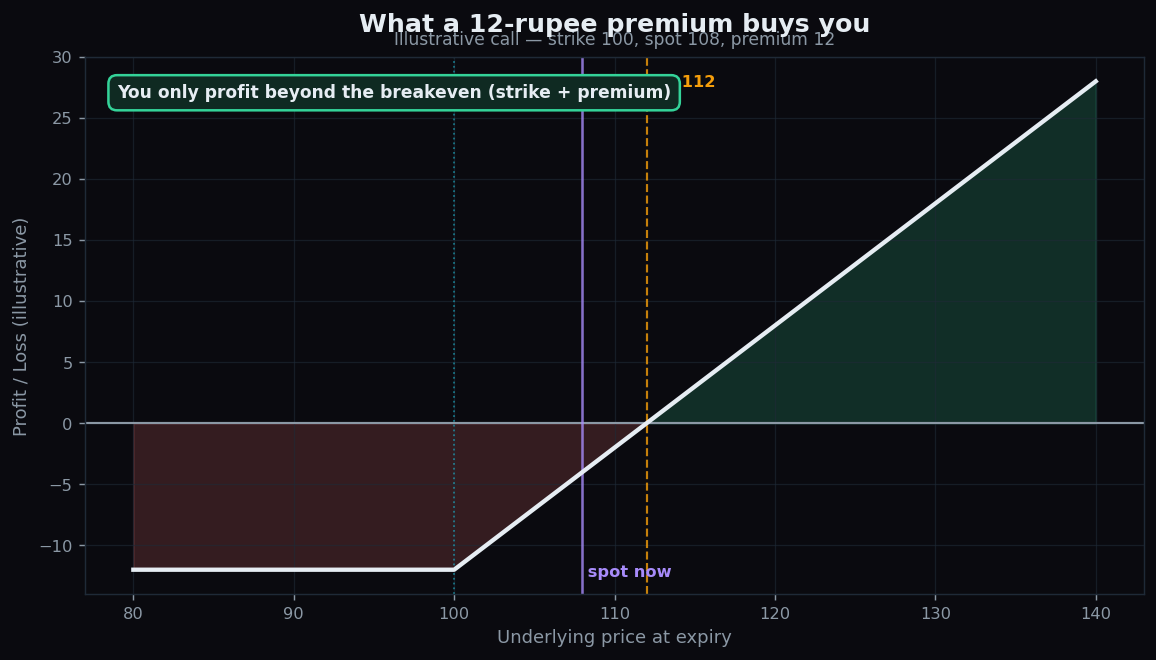

Let us price one option from scratch. A stock trades at 108. You look at a call with a strike of 100, quoted at a premium of 12.

- Intrinsic value = 108 − 100 = 8 (the option is in-the-money by 8).

- Time value = 12 − 8 = 4 (the rest of the premium).

- Breakeven = strike + premium = 100 + 12 = 112.

So even though the option is already in-the-money, the stock must climb past 112 before you turn a net profit, because you paid 4 of time value on top of the 8 of intrinsic worth. That gap between the current price and the breakeven is the time value laid bare. This is an illustration of the mechanics, not a recommendation to trade.

What drives the premium up and down?

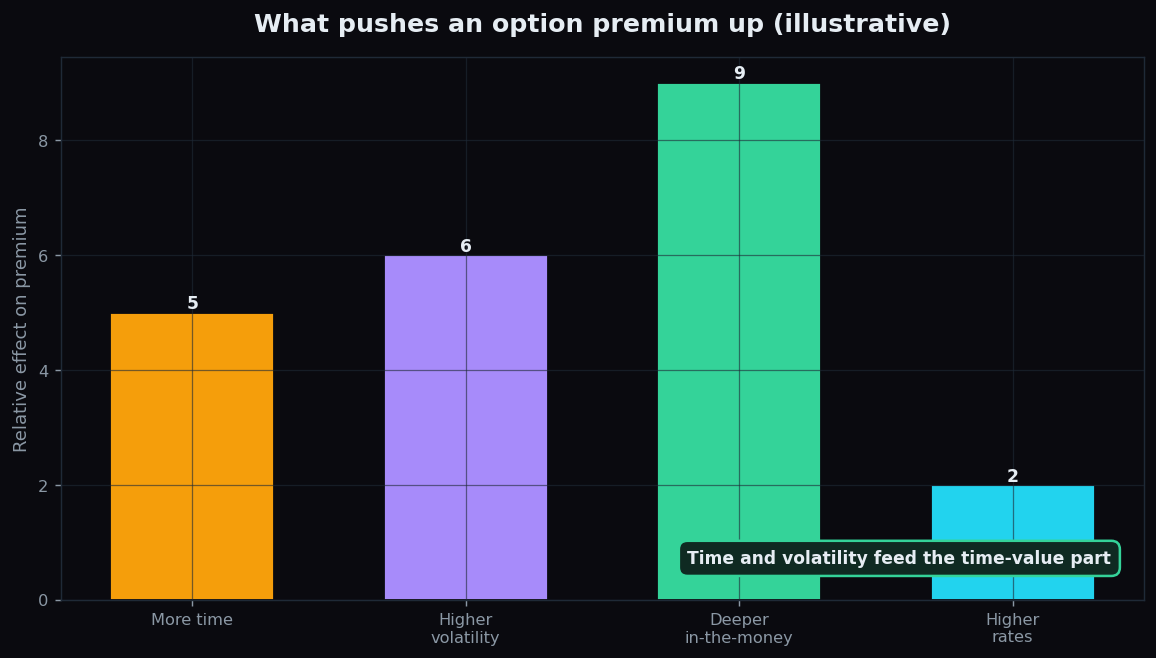

Intrinsic value moves only with the price of the underlying — it is mechanical. Time value is where the interesting forces live. Four main factors push a premium around:

- Time to expiry. More days left means more time value. As expiry nears, time value shrinks toward zero.

- Volatility. The single biggest driver of time value. When the market expects big swings, options cost more, because a large move is more likely. When calm returns, premiums deflate — a phenomenon worth understanding through our explainer on why an option can lose value even when you were right.

- Moneyness. The deeper in-the-money an option, the more intrinsic value it carries, so the higher the total premium.

- Interest rates. A smaller, slower influence, but rising rates nudge call premiums up and put premiums down.

The honest catch

The dangerous half of the premium is time value, because it is not yours to keep. Every day that passes, time value drains away — a process called time decay — and at expiry it reaches exactly zero. An option left holding only time value, with no intrinsic value, expires worthless.

This is why option buyers can be right about direction and still lose money. If you pay 12 for an option that is mostly time value and the stock barely moves, that time value melts and your option is worth less even though nothing went against you. Volatility can betray you too: buy when premiums are bloated by fear, and a return to calm can shrink your option's value overnight. Always know how much of the premium you are paying is real intrinsic worth and how much is fragile, decaying possibility.

Knowing what you are actually paying for is the difference between gambling and informed learning. TrueTrend turns live option pricing into plain-language context built for beginners. Create a free account to explore how premiums behave.

Key takeaways

- The premium is the price of an option, paid up front, and a buyer's maximum loss.

- Premium always splits into intrinsic value + time value.

- Intrinsic value is the immediate exercise worth (never below zero); time value is the price of remaining possibility.

- Volatility and time to expiry are the biggest drivers of time value.

- Time value decays to zero by expiry — so being right on direction is not enough.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.