IV Crush Explained: Why Your Right Option Still Lost Value

You bought a call before the results. The index moved up, exactly the way you guessed. And your option still lost money. That stings — you were right and the market paid you a penalty for it. The usual culprit has a name: IV crush. Once you see how it works, that confusing loss turns into something you can predict and plan around.

First, what is an option actually worth?

An option is a contract that pays off if price moves your way; the price you pay for it is the premium. That premium is built from two separate parts, and keeping them apart is the whole secret here.

- Intrinsic value — the part that is already “in the money.” If you own a call to buy at 24,000 and the index is at 24,100, that call has 100 points of intrinsic value. Real, locked-in.

- Extrinsic value — everything else you pay on top. It is the price of hope and time: the chance the move gets bigger before expiry. Traders also call it time value.

Implied volatility (IV) is the engine behind that extrinsic part. IV is the amount of future movement the option market is currently pricing in — the crowd’s guess at how wild the ride will be. High IV means traders expect big swings, so they pay up for options. Low IV means calm is expected, so options get cheap.

The two parts — and why one of them vanished

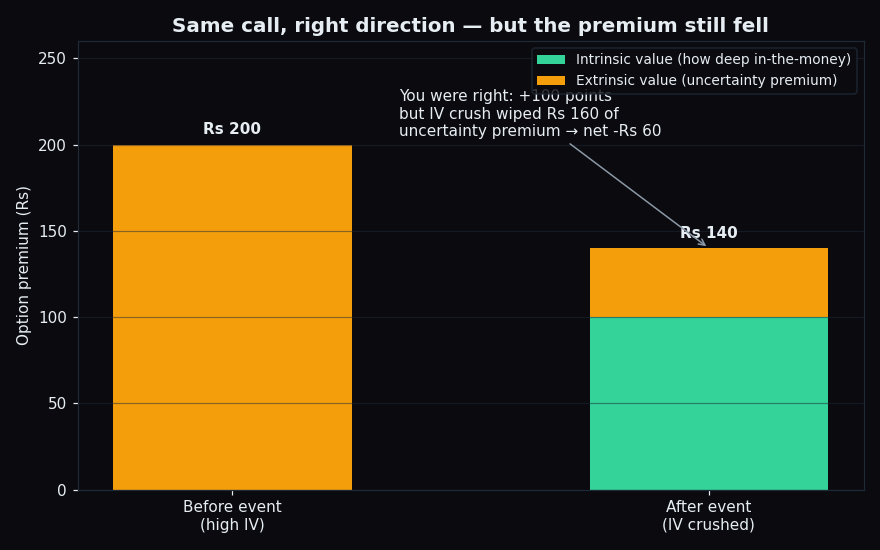

Here is the picture that explains your loss. Imagine the index at 24,000 and you buy the at-the-money (ATM) call — the strike nearest the current price, here 24,000 — the day before a big event. Because nobody knows what the event will bring, IV is high (say 40%) and the option costs ₹200. At that moment it is all extrinsic value: the index is sitting right at the strike, so intrinsic value is zero. You are paying ₹200 purely for uncertainty.

The event passes. The index rises 100 points to 24,100 — you were right. Your call now has 100 points of intrinsic value. But the uncertainty is gone, so IV collapses from 40% to 16%, and the extrinsic value shrivels from ₹200 to about ₹40. Add it up: 100 intrinsic + 40 extrinsic = ₹140. You paid ₹200, the option is worth ₹140, and you lost ₹60 — while being completely right about direction. That gap is IV crush: the air rushing out of the extrinsic part faster than the move could fill it.

Why the air goes in before an event and rushes out after

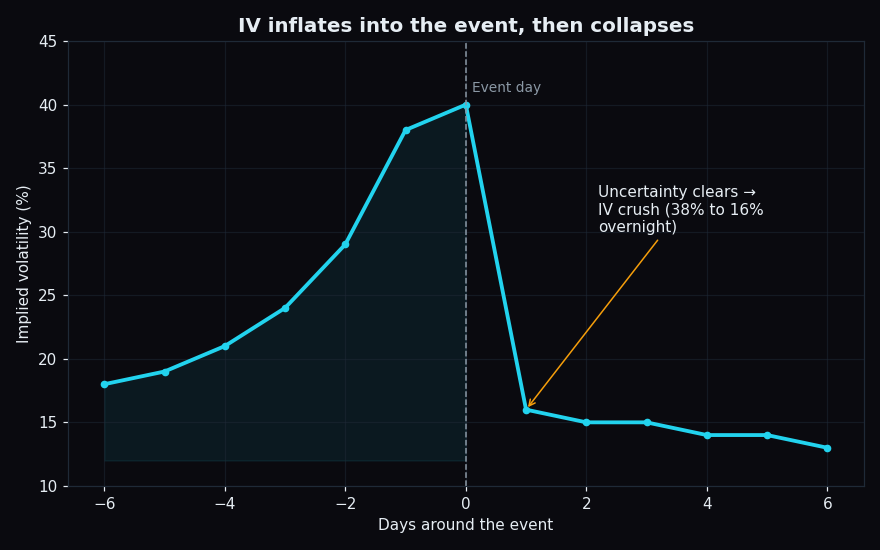

Think of an option like insurance on price, and IV as the storm forecast. When a cyclone is on the radar, house insurance gets expensive — everyone wants protection at once. The morning after the storm passes, that fear premium disappears overnight, even if the winds did pick up a little. The danger is no longer unknown, so nobody will pay extra for the unknown.

Options work the same way. Before a budget, an RBI policy decision, an election count, or a heavyweight earnings day, traders bid options up because anything could happen — IV climbs. The moment the news is out, the biggest question mark is resolved. IV deflates in a single session, and every option carrying extrinsic value loses a chunk of it at once.

This is why the timing of your trade matters as much as the direction. Buy into a wall of rising IV and you are paying top price for the forecast right before it expires.

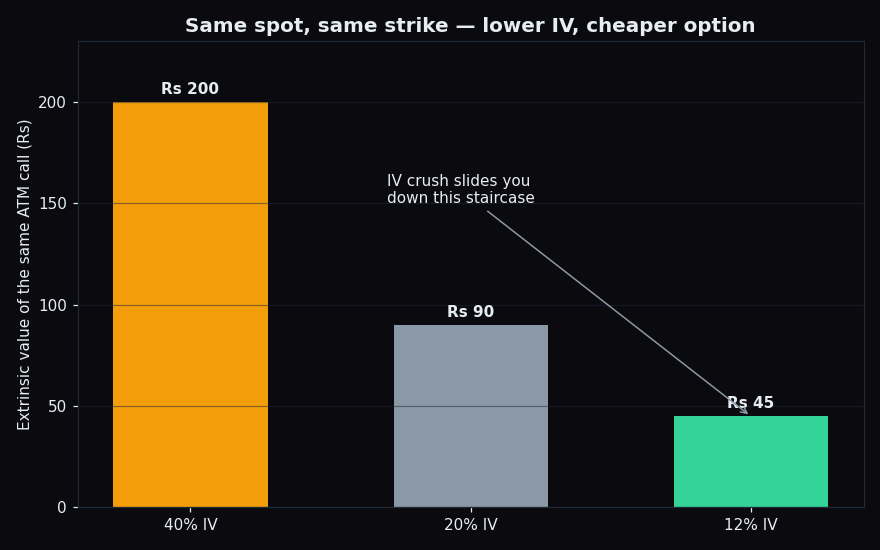

Same index, same strike — just a cheaper option

To really feel it, hold everything still except IV. Same index level, same ATM strike, same days to expiry — only the implied volatility changes. The extrinsic value rises and falls in lockstep with IV.

Nothing about the index changed in that chart — not the price, not the strike. Only the expected wildness fell, and the option got cheaper for it. IV crush is just sliding fast down this staircase in one go. It is the same engine that sets the day’s expected move, the range option prices imply; if that idea is new, see how option prices reveal the day’s likely range.

How market participants read it

IV crush is context, not a call to act. A few common, descriptive uses:

- Knowing what you are paying for. Before an event, a fat premium is mostly extrinsic value — a bet that the move beats what is already priced, not just that it happens.

- Separating “right” from “paid.” Being right on direction and making money are two different things once IV is in the mix. The move has to clear both the strike and the premium you paid.

- Reading the whole option picture. IV sits alongside other option-structure reads, like where heavy positioning clusters. If that is new, start with what open interest is and why it matters.

The honest catch

The deeper lesson behind IV crush is humbling: in options, a correct guess about direction is necessary but not sufficient. Volatility, time, and the price you paid all get a vote. Markets rarely behave as tidily as a single forecast hopes.

You can see that resistance to prediction in our own measured data. On the public scoreboard, the Nifty closed within one strike of its max-pain level — the option market’s strongest “gravity” point — in just 38% of 52 scored sessions, and Bank Nifty in only 8% of 51. Even the most-watched magnet pins the close a minority of the time. The takeaway is not pessimism; it is respect for how much structure, not just direction, drives an outcome.

Key takeaway: an option’s premium is intrinsic value plus a fragile uncertainty premium. When implied volatility collapses after an event, that uncertainty premium can vanish faster than a correct move can replace it — so you can be right on direction and still lose.

TrueTrend turns this kind of option-structure read — implied volatility, expected move, and where positioning clusters — into a clear, at-a-glance picture across Nifty, Bank Nifty and F&O, and scores how its own levels actually played out, in public. See the daily read on TrueTrend.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.