Option Theta: Time Decay Explained for Beginners

Have you ever held an option, seen the underlying go almost nowhere, and still watched the premium shrink day after day? You were not imagining it. You were watching theta — the option Greek that measures how much value an option loses simply because time is passing. If delta is the option’s speed and gamma is its acceleration, theta is the quiet tax the clock charges every single day.

What theta actually measures

Theta is the sensitivity of an option’s premium to the passage of one day, holding everything else still. It is usually written as a negative number for option buyers. A theta of −5 means that, if nothing else changes, the option’s premium will be about 5 lower tomorrow than it is today, purely because one day has elapsed.

To see why, split an option’s premium into two parts:

- Intrinsic value — the part that is “already in the money”. For a call, it is how far the underlying sits above the strike (never less than zero).

- Time value — everything else: the extra you pay for the possibility that the option moves further into the money before expiry.

Theta eats the time value. As expiry nears, there is less and less time for a favourable move, so that hope-portion of the premium drains away. At expiry, time value is exactly zero — only intrinsic value remains.

The melting ice cube analogy

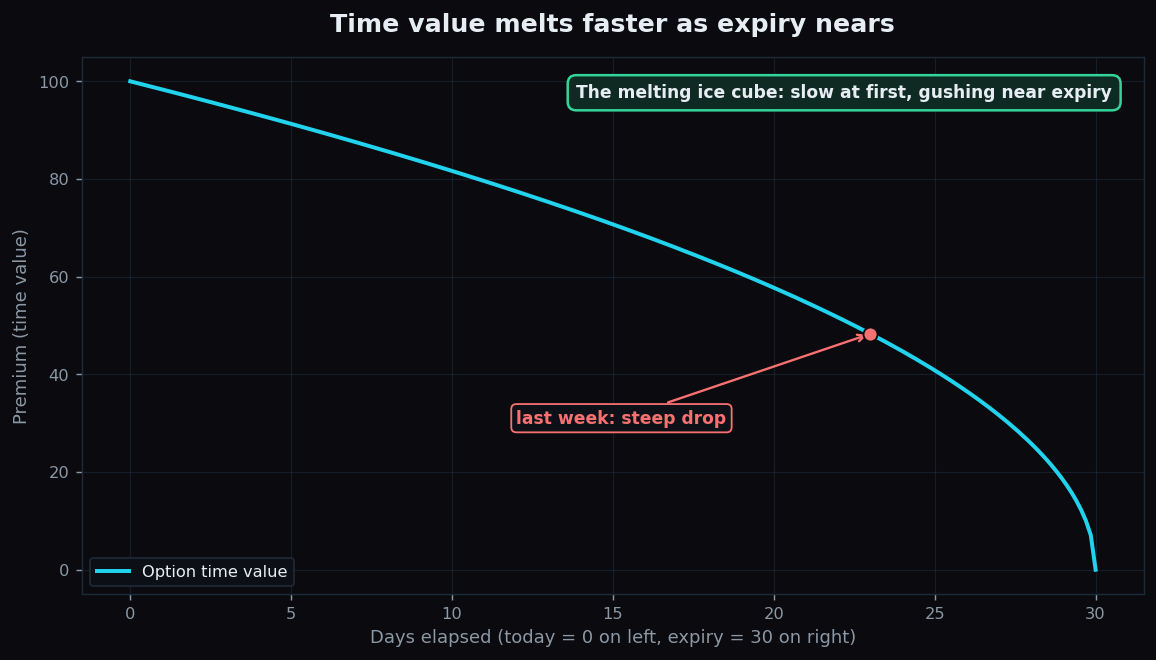

Picture the time value of an option as an ice cube sitting on a table. It melts a little every hour whether or not anything dramatic happens in the room. On a cool morning (far from expiry) it melts slowly. As the day warms (expiry approaches) it melts faster and faster, and in the final hour it is mostly a puddle. An option buyer owns that ice cube. The seller, in effect, is paid to watch it melt.

The curve above is the shape every option buyer should burn into memory. Time value does not bleed away in a straight line. It declines gently at first, then drops off a cliff in the last stretch before expiry. The decay accelerates.

Why decay speeds up near expiry

For an at-the-money option, time value behaves roughly like the square root of the time remaining. That has a striking consequence: going from 30 days to 20 days costs relatively little, but going from 10 days to 1 day costs a great deal. The same option loses far more value in its final week than in any earlier week.

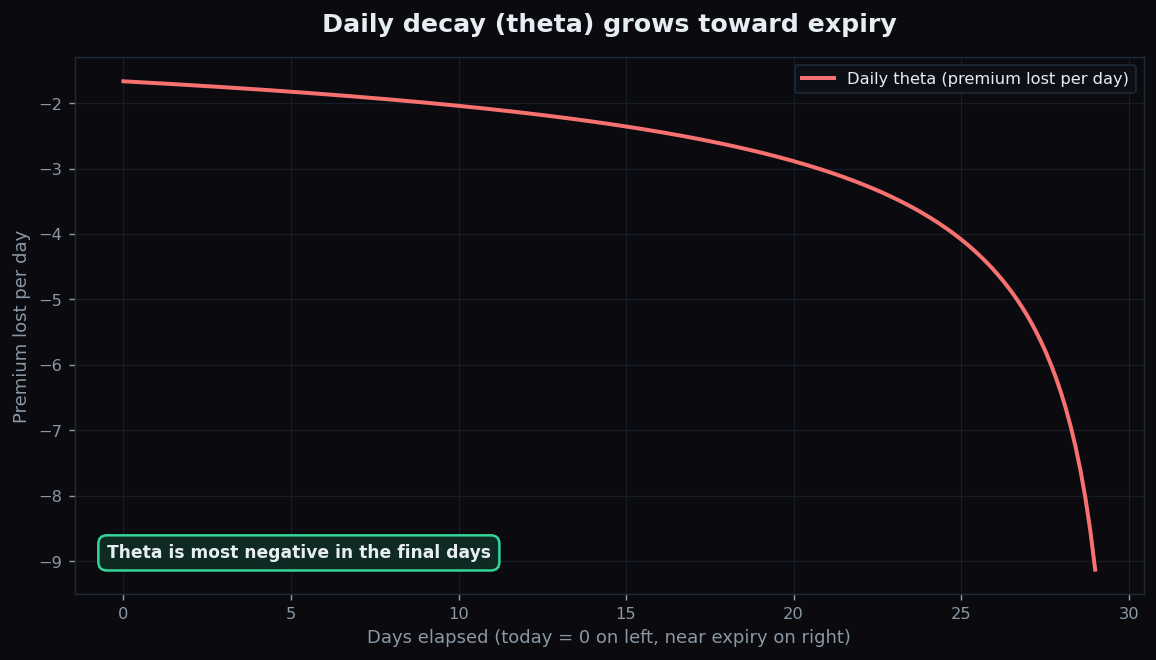

The second chart shows the daily bite directly. Theta — the amount lost each day — starts small and grows steadily larger (more negative) as expiry approaches. The last few days carry the heaviest decay. This is why holding a near-expiry option through a quiet, sideways market is so frustrating: the clock charges its highest rent exactly when there is least time for the market to bail you out.

A worked example with round numbers

Suppose an index is at 20,000 and you purchase an at-the-money call for a premium of 100, with 30 days to expiry. Because it is exactly at-the-money, that entire 100 is time value — there is no intrinsic value yet.

- With 30 days left, daily theta might be about −2. A quiet day shaves the premium from 100 to roughly 98.

- With 10 days left, the same option’s theta might be about −4. A quiet day now costs around 4.

- With 2 days left, theta might be −9 or more. A quiet day can wipe out a big chunk of what remains.

The point is not the exact figures, which are illustrative. It is the trajectory: the daily cost of simply holding the option rises as expiry approaches. The underlying did not have to move against you at all for the position to lose ground.

Why theta matters

- It sets the hurdle for buyers. When you purchase an option, the underlying must move enough, and soon enough, to outrun the time decay. Theta is the headwind your view has to beat. A correct but slow call can still lose.

- It is the seller’s income. Every rupee of time value a buyer loses to theta is, broadly, a rupee an option seller collects — in exchange for taking on risk if the market moves sharply. Time decay is the engine behind option-writing strategies.

- It explains “right but still down” trades. Pair theta with a drop in implied volatility and you get the classic premium collapse explained in why an option can lose value even when you were right.

The honest catch

- Theta is not the same for every option. At-the-money options carry the most time value and therefore the steepest decay. Deep in-the-money options are mostly intrinsic value, so they decay less. Far out-of-the-money options have little time value left to lose.

- Theta assumes nothing else moves. It is the decay on a still day. A strong move in the underlying (delta and gamma) or a jump in implied volatility (vega) can swamp theta entirely — for better or worse.

- Decay is not evenly spread within a day either. Around weekends and holidays, several days of time value can come out at once, which can surprise buyers who only watch the screen during market hours.

- Selling to collect theta is not free money. The seller earns steady decay but is exposed to fast, large moves — the unfavourable side of gamma. The income is real; so is the tail risk.

Want to understand how time, positioning, and expiry pressure shape the option chain — explained for learners, not insiders? TrueTrend turns that structure into plain-English context. Create a free TrueTrend account to keep learning.

Key takeaways

- Theta = the melting ice cube: how much premium an option loses for one day passing, all else equal.

- Theta drains time value, not intrinsic value; at expiry, only intrinsic value is left.

- Decay accelerates near expiry — the final week sheds far more value than earlier weeks.

- At-the-money options carry the steepest theta; deep-ITM options decay the least.

- Theta is a headwind for buyers and income for sellers — but neither side gets it without taking on real risk.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.