The Covered Call Explained (Illustrative Example)

The covered call is one of the first option strategies most people meet, because it starts from something you may already own: shares. You hold the stock, you sell one call option against it, and in return you collect a small upfront payment. In exchange, you agree to a ceiling on how much you can gain if the stock shoots up. This article walks through the mechanics with simple round numbers. It is an illustrative example to explain how the structure works — not a recommendation, and not a trade to place.

What a covered call actually is

First, two definitions. A call option is a contract that gives its buyer the right to buy a stock at a fixed price (the strike) before the contract expires. The person on the other side — the seller or writer — takes the opposite obligation: if the buyer exercises, the writer must hand over the shares at that strike. For taking on that obligation, the writer is paid a premium upfront.

A covered call simply means you write (sell) a call while already owning the underlying shares. The word “covered” is the key. If the buyer ever demands the shares, you already have them sitting in your account, so you are covered. Contrast that with a “naked” call, where the seller owns nothing and would have to buy shares at any price to deliver — a far riskier position.

Think of it like owning a flat and renting out a purchase option to a tenant. They pay you a fee today for the right to buy your flat at a set price later. You keep the fee no matter what. If they never buy, you simply keep both the fee and the flat. If they do buy, you must sell at the agreed price, even if the market has since risen higher.

A worked example with round numbers

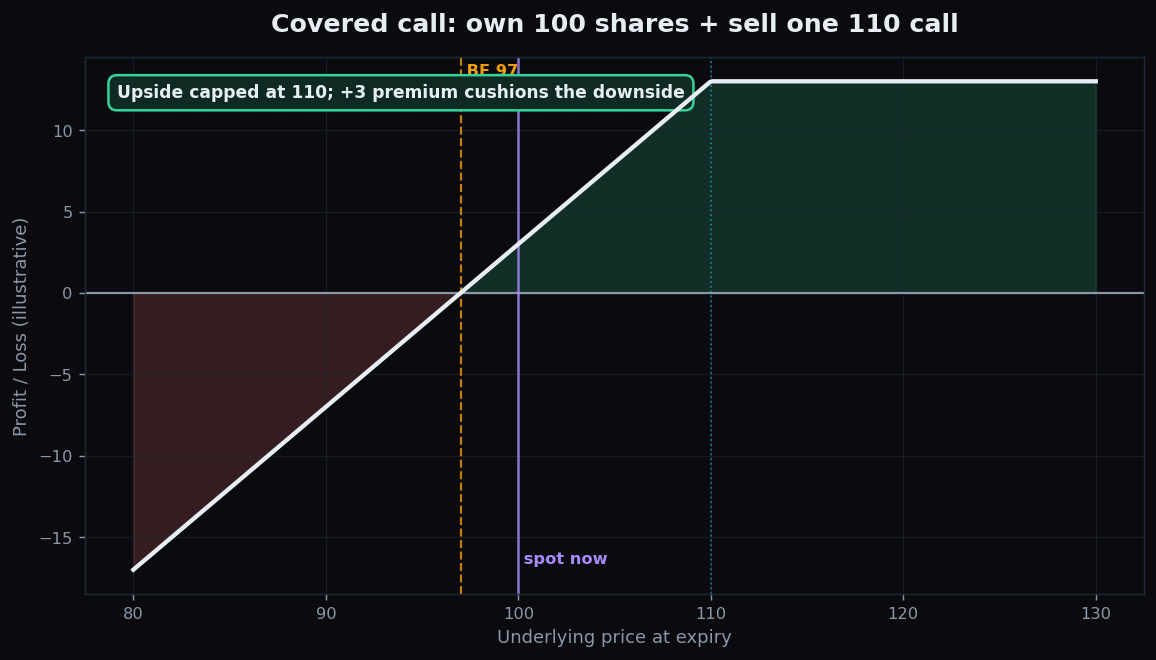

Imagine you own 1 lot of a stock trading at 100. You sell one call with a strike of 110 and receive a premium of 3 per share. Three outcomes at expiry:

- Stock stays at 100. The 110 call expires worthless to its buyer. You keep your shares and pocket the 3 premium. Your effective cost on the shares is now like 97.

- Stock rises to 110 or above, say 120. The buyer exercises. You must sell your shares at 110. Your gain is the 10 points from 100 to 110, plus the 3 premium, for a total of 13. But notice: had you not sold the call, you would have captured the full move to 120. The premium was the price of giving up that extra upside.

- Stock falls to 90. The call expires worthless, so you keep the 3 premium. But your shares are now worth 90. The 3 you collected softens the blow, but it does not stop the loss.

So the maximum profit is capped at 13 (reached at the 110 strike and above), the breakeven is 97 (your 100 entry minus the 3 premium), and the downside is still essentially the same as owning the stock, just cushioned by 3.

Why people study it

The covered call is popular as a teaching tool because it shows a clean trade-off. You are converting some uncertain future upside into certain cash today. For an investor who already owns shares and believes the stock is unlikely to surge in the short term, the premium is income earned on an asset they are holding anyway. The position also slightly lowers the breakeven, which is why some describe it as a way to reduce cost basis over time.

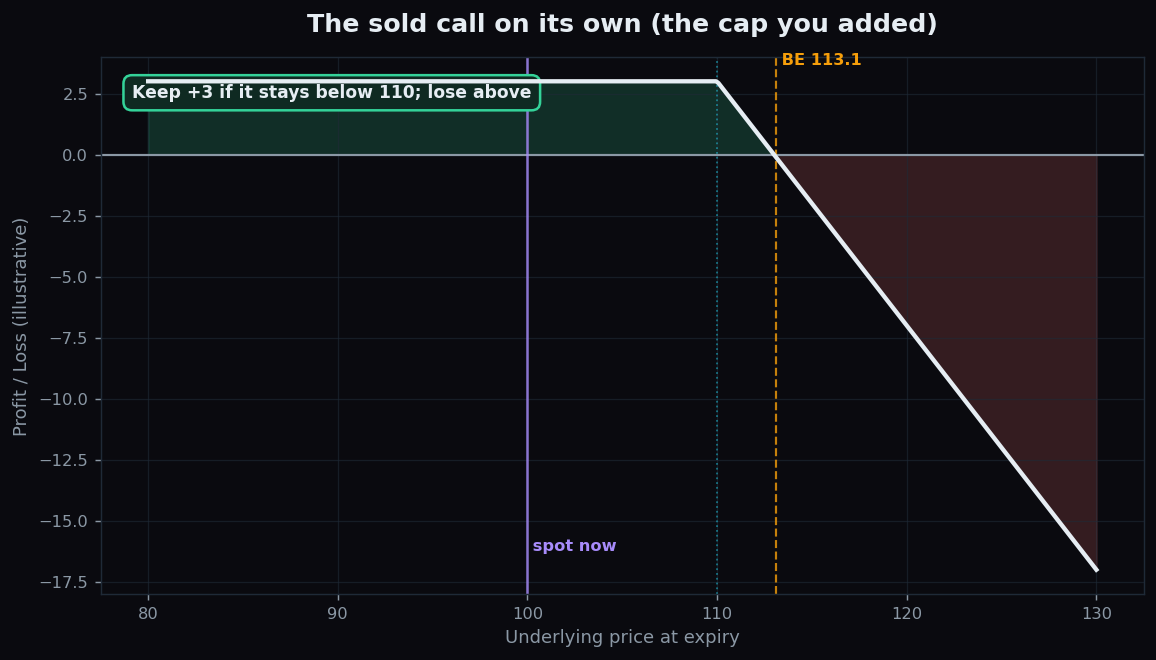

The two charts below separate the pieces. The first showed the combined position. The second shows the sold call on its own — the part you bolted on top of your existing shares to create the ceiling.

The honest catch: what can go wrong

No structure is free, and a covered call has real downsides worth naming plainly:

- Your upside is capped. If the stock doubles, you do not. You still sell at 110. The single worst feeling in this strategy is watching a big rally that you no longer fully participate in.

- The downside is barely protected. If the stock collapses to 60, the 3 premium is almost meaningless. A covered call is not a hedge; the protection it offers is tiny. For real downside cover, people study the protective put instead.

- You can be assigned early. The buyer may exercise before expiry, especially around dividends, forcing you to give up the shares sooner than planned.

- Opportunity and tax friction. Selling the shares on assignment may trigger taxes or break a long-term holding you wanted to keep.

Premium also shrinks when markets are calm. When implied volatility is low, the cash you receive for selling the call is smaller — the same idea explored in how implied volatility affects option prices.

Want to see how a stock is actually positioned — where the big option open interest sits and how the daily range is shaping up — before you ever think about structures like this? TrueTrend turns raw option data into plain-English context. Explore TrueTrend free and learn to read the market structure first.

Key takeaways

- A covered call is owning shares and selling one call against them, collecting a premium upfront.

- In the example: own at 100, sell the 110 call for 3 → max profit 13, breakeven 97, upside capped above 110.

- It trades uncertain upside for certain cash today, and slightly lowers your breakeven.

- The catch: upside is capped, downside is only lightly cushioned, and early assignment is possible.

- This is an educational illustration of the mechanics, with made-up numbers — not advice and not a trade to place.

See these concepts on live market data — free

Create a free TrueTrend account to watch daily support/resistance levels, market regime, and option-positioning charts on NIFTY, BankNifty and 12 more instruments. Every level we publish is scored on a public scoreboard — misses included. No card required.

Free forever tier · daily levels with published hit-rates across every instrument. Descriptive market structure, not investment advice.

Not ready for an account? Get the daily levels by email.

One short email each market day — the indices' call wall, put wall, gamma flip and max pain, and how the last session's levels scored. Free, no account, unsubscribe anytime.

Descriptive market structure, not investment advice. We never share your email.